How people are preparing for retirement: Survey insights

How people are preparing for retirement: Survey insights

Retirement is an important financial milestone that typically takes decades of planning and saving to reach. And there are many decisions to be made along the way: When should you start saving? How much will you need? How much should you set aside each month? When should you retire? Uncertainty about the market and a rising cost of living can turn up the pressure and further complicate the process.

So how are we doing?

SoFi surveyed 500 U.S. adults aged 18 or older in April 2024 to find out how Americans are grappling with these and other tricky retirement issues. We asked them when they started saving, how much progress they’ve made toward their goals, and how confident they feel in their ability to retire comfortably. Here’s what we learned.

Key findings

Some of the highlights of SoFi’s 2024 Retirement Survey include:

- Just 7% have $500,000 or more saved for retirement.

- Around 1 in 2 contribute less than 10% of their income to their retirement savings.

- The majority of savers plan to retire at age 60 or older.

- 12% expect to retire by age 49.

- 31% are relying on Social Security to be their primary source of income in retirement.

- 35% are very confident they will be able to retire on time, while 33% are somewhat confident.

Retirement readiness

Retirement readiness can be interpreted as having enough saved to cover expenses for the rest of your life once you stop working. So, how prepared are Americans? Here’s what our survey results tell us.

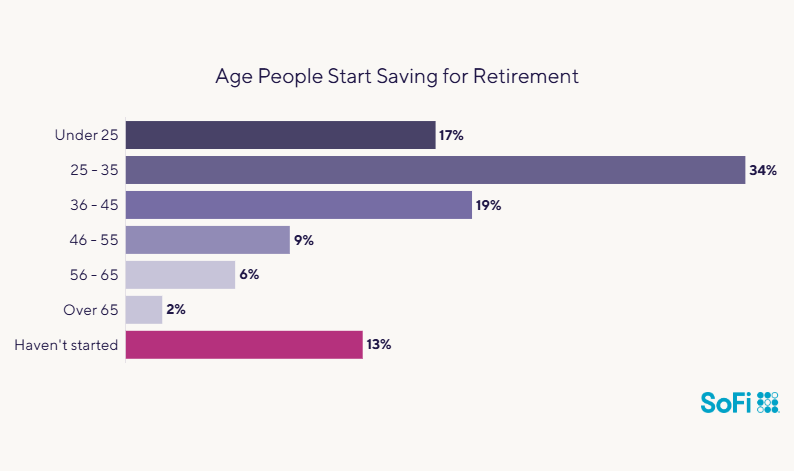

51% of Americans start saving before age 35

About 1 in 3 respondents said they started saving for their golden years between the ages of 25 to 35, while 17% began before age 25. That’s a positive sign, as getting an early start means more time to capitalize on the power of compounding returns. However, roughly 1 in 3 adults said they didn’t start saving until after the age of 36, and 13% said they had yet to put a retirement plan into action.

SoFi

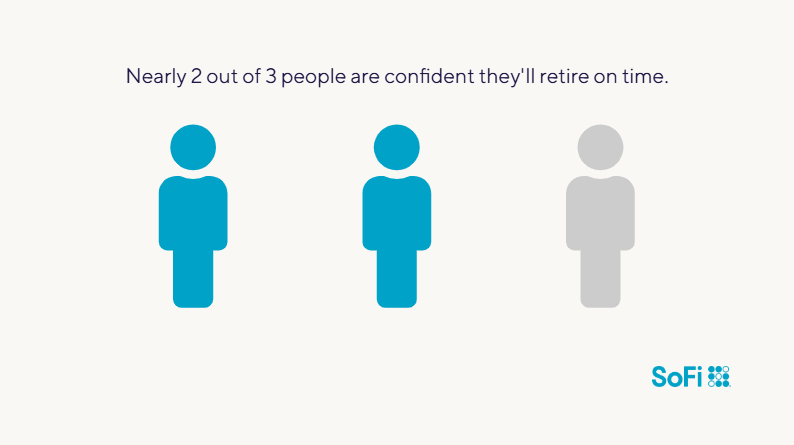

2 out of 3 are somewhat or very confident they will be able to retire on time

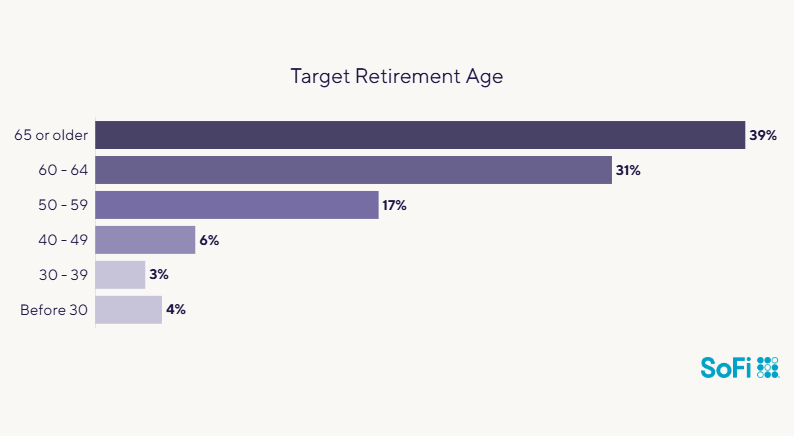

Nearly 40% of respondents hope to retire at age 65 or older, while 31% are looking to exit the workforce between ages 60 and 64. Roughly 30% are setting their sights on retiring before the age of 60, and close to 12% are aiming to retire by age 50.

SoFi

How confident are they in meeting these goals? A full 68% are very or somewhat confident in their ability to retire at their target age. Only 15% were somewhat or very doubtful they’ll be able to retire on time; 17% said they feel neither confident nor doubtful.

SoFi

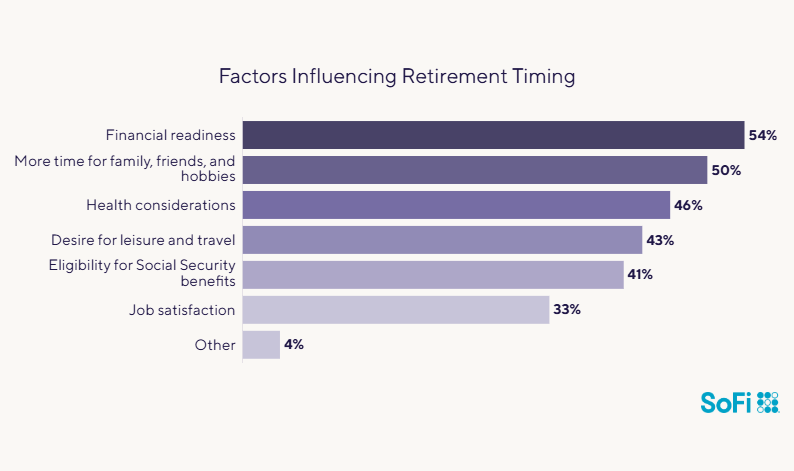

54% say financial readiness is a key reason to retire

How do people decide when to retire? Financial readiness — in other words, being able to afford to retire — is the top consideration, according to our survey. However, it’s not the only one.

Other major reasons why people want to retire by a certain time include (in order of importance): being able to spend more time with friends and family and engage in hobbies; health considerations; a desire for leisure and travel; and eligibility for Social Security benefits. Last but not least: 1 in 3 adults say job satisfaction (or lack thereof) is influencing their decision on when to retire.

SoFi

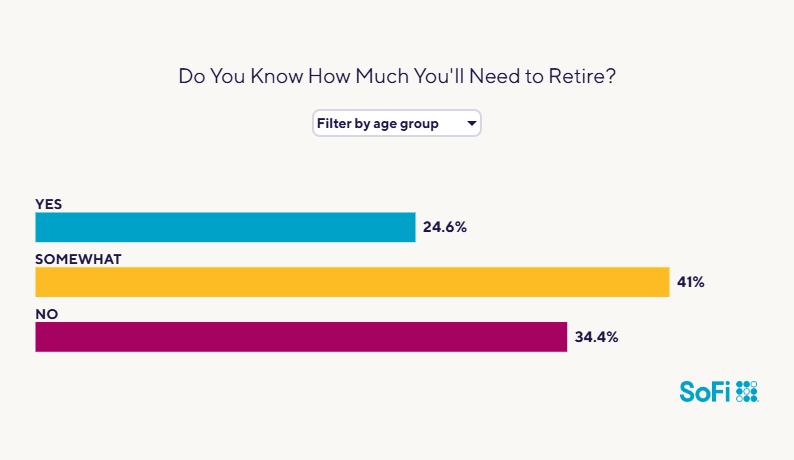

75% of adults don’t know how much they’ll need to retire

Americans want to retire and they have a good idea when they want to do it, but most haven’t figured out exactly how much money they’ll need to make it happen. In SoFi’s Retirement Survey, just 1 in 4 respondents said they have calculated exactly how much they’ll need to exit the workforce for good and have a detailed plan in place. The remainder either have a general idea of how much they’ll need to retire comfortably (41%) or don’t know and haven’t done any calculations (34%).

SoFi

Of the 34% who don’t know how much money they’ll need to retire, roughly 40% are aged 45 or older, which could spell trouble if they’re underfunding their retirement accounts.

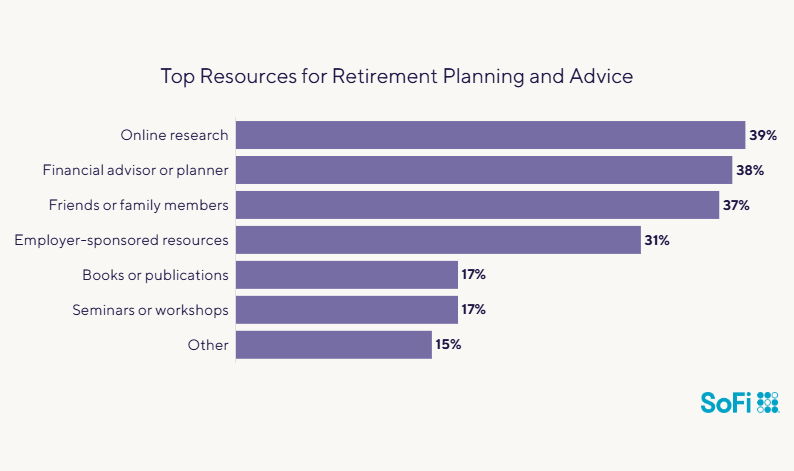

4 in 10 Americans learn about retirement planning online

Retirement is a complex topic and it helps to have resources to guide you through the planning process. According to our study, the internet is America’s top choice for retirement research and information, relied on by nearly 40% of respondents. Following close behind (in order of preference): professional financial planners/advisors (38%), friends and family (37%), and employer-provided resources (31%).

A smaller number (17%) turn to books and other publications, and the same percentage (17%) looks to seminars and workshops to get guidance on retirement planning.

SoFi

Retirement saving habits and strategies

Money habits can make a difference when attempting to move the needle on retirement. Unfortunately, many American workers aren’t doing enough to reach their retirement goals. Here’s a look at how much our respondents are putting aside and how much they have amassed so far.

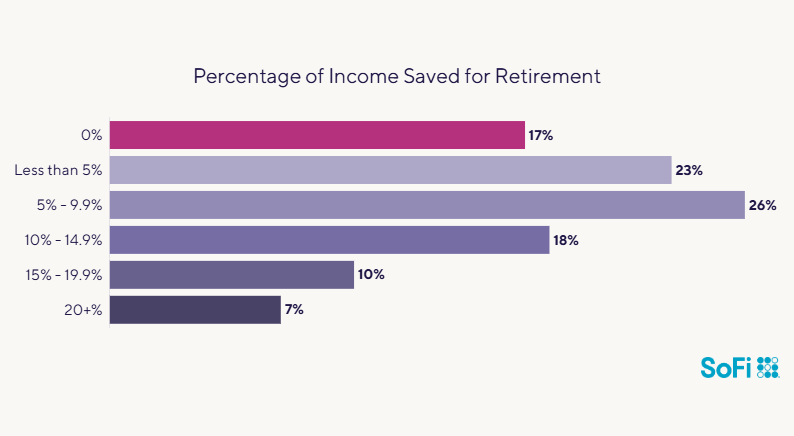

Just 17% are putting at least 15% of their income toward retirement

Financial advisors generally recommend saving at least 15% of your pre-tax income each year for retirement. Unfortunately, only 17% of respondents in SoFi’s Retirement Survey are following that advice. More concerning: Nearly half of the respondents are contributing less than 10% of their income to retirement.

Those that are contributing 15% or more are more likely to be high-income earners in the earlier stages of their careers. Fifty percent of those who contribute 15% or more have a household income of at least $100,000 and 60% are aged 25 to 44.

SoFi

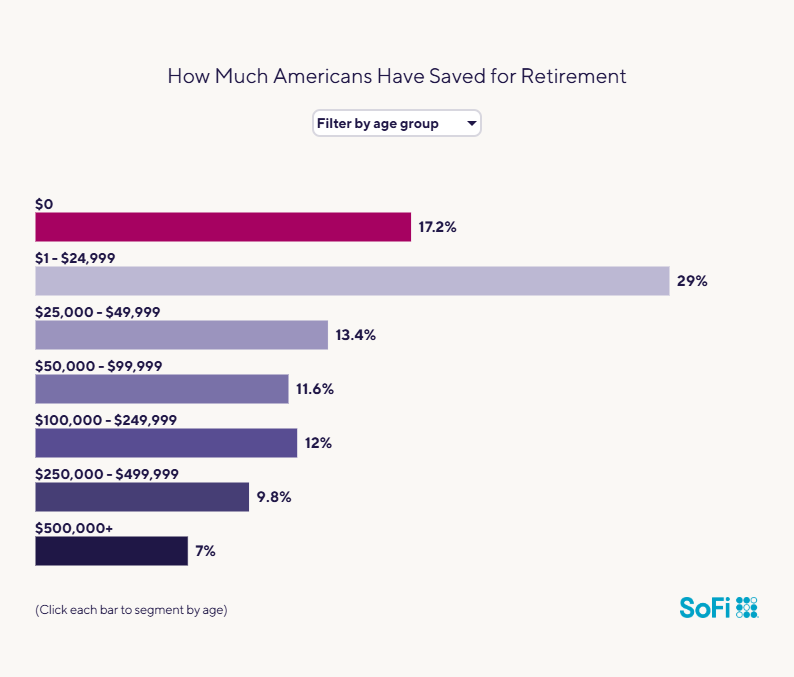

17% have no retirement savings

A common guideline is to save at least one times your salary by 30, three times by 40, six times by 50, eight times by 60, and 10 times by 67.

However, our survey suggests that many Americans may not be making those milestones. Around 40% have less than $50,000 saved for retirement. Only 22% have put aside between $100,000 and $500,000, and a scant 7% have more than $500,000 in retirement savings.

Those that have at least $100,000 saved for retirement are more likely to be men, have a college or higher degree, and be married or living with a partner. Those with less than $100,000 stashed away for their retirement years tend to be women, have a high school level education level or lower, and single, divorced, or widowed.

SoFi

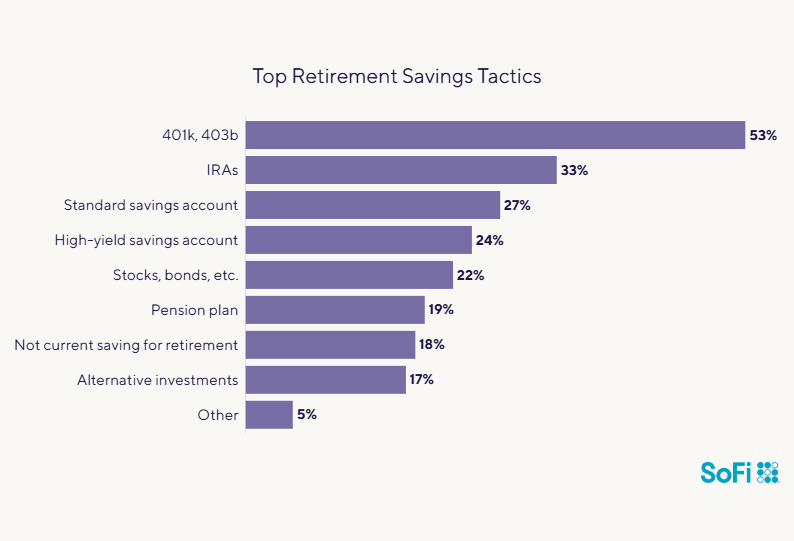

53% save for retirement at work

Workplace plans, like 401(k) or 403(b) plans, offer a tax-advantaged way to save for retirement, and the majority of the Americans we surveyed are using them. A smaller number, 19%, said they have a pension plan, while 33% have an individual retirement account (IRA), such as a Roth IRA.

SoFi

Twenty-four percent of respondents include high-yield savings accounts in their retirement plan, while 27% are using traditional savings accounts. Only 17% put retirement funds in alternative investments like real estate or gold.

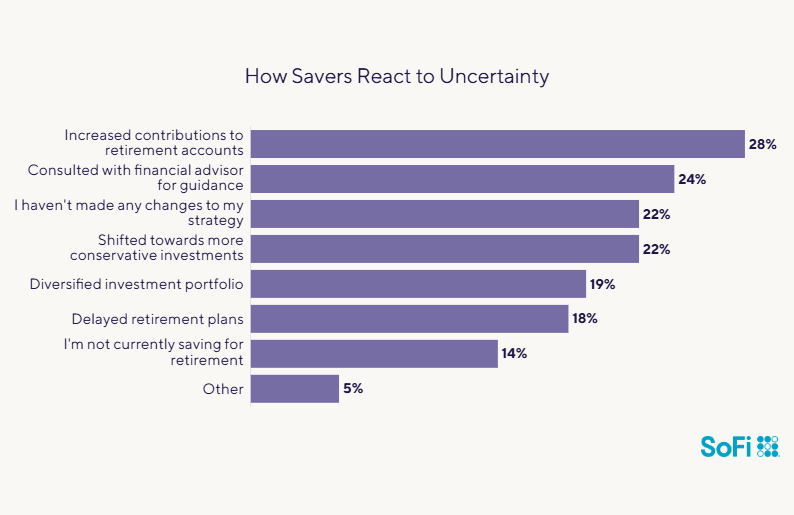

28% step up retirement saving during uncertain time

Market volatility and economic instability deter some savers (about 1 in 5) from making retirement contributions. However, a fair number of Americans (28%) actually increase contributions to retirement accounts in response to economic uncertainty. Others simply adjust their investment strategy: 22% shift toward more conservative investments, while 19% focus on diversifying.

SoFi

Early retirement and financial independence

Many Americans dream of early retirement, which generally means before the standard age of 65 to 70. It’s a lofty goal and typically requires getting an early start on saving, while minimizing expenses and debt.

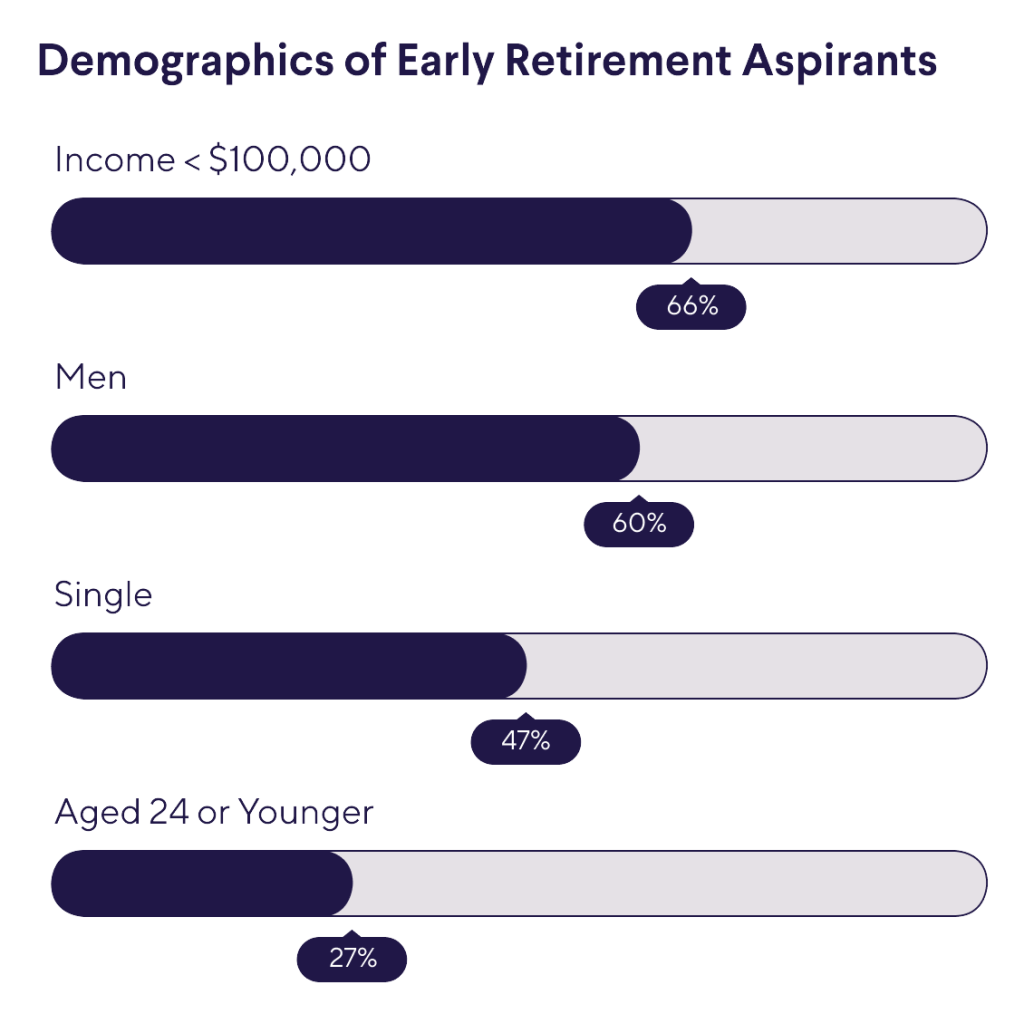

12% aim to retire before age 50

As mentioned above, a modest 12% of Americans want to retire at age 49 or younger. Of that group:

SoFi

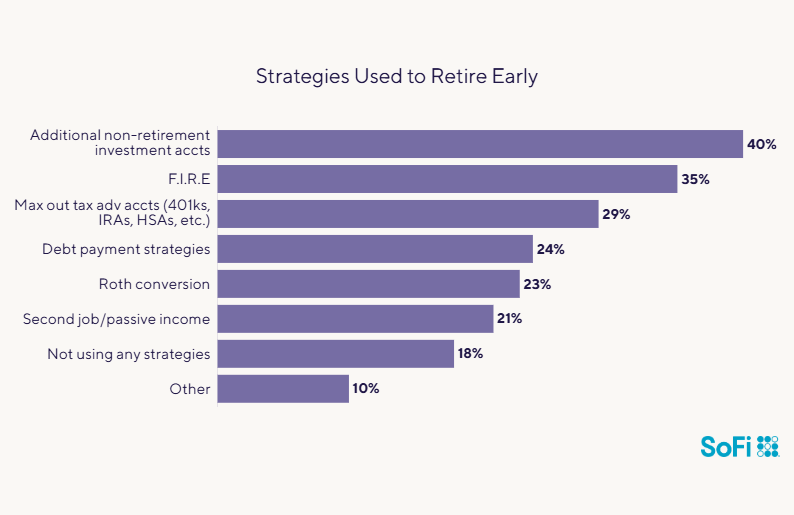

Roughly 1 in 3 Are Using FIRE strategies

Of those who said they want to retire before they turn 50, about a third (36%) are using the Financial Independence, Retire Early approach, a financial movement that embraces frugal living, aggressive saving, and investment. Others are working to get there by maxing out their retirement plans, using brokerage accounts, aggressively paying down debt, or generating extra income through a second job or passive income strategies.

SoFi

Retirement income and Social Security

Retirees generally rely on multiple resources, including investments, part-time work, and Social Security, to ensure a sustainable income stream in their retirement years. Most of our survey respondents are planning for that. However, some are counting solely on Social Security for their retirement years.

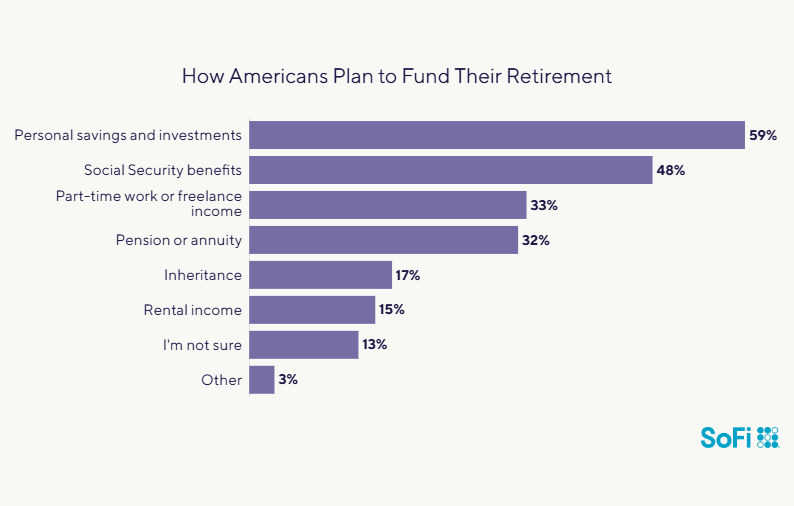

60% plan to use their savings to fund their retirement

According to our survey, today’s workers are mostly counting on their investments (like their 401(k)s and IRAs to fund their retirement. Nearly half are also relying on Social Security benefits, and 32% expect some income from pensions or annuities. Roughly 1 in 3 also plan to supplement their savings with part-time work or freelancing. A full 13% aren’t yet sure how they’ll fund their retirement.

SoFi

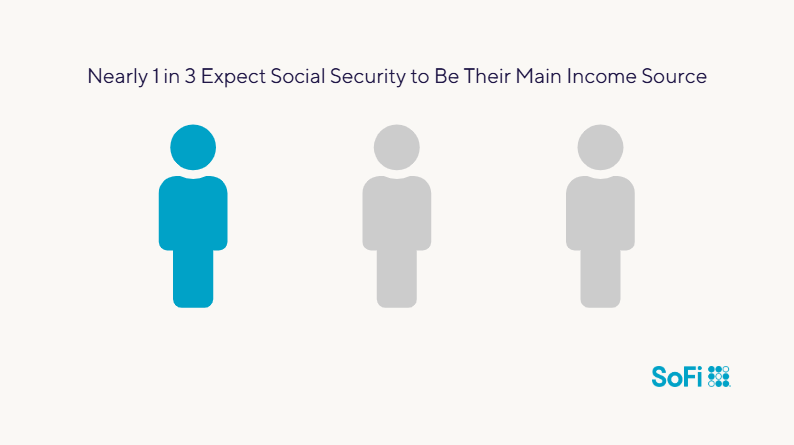

Nearly 1 in 3 expect Social Security to be their main income source

Social Security is a federal program that was designed to help people pay their expenses during retirement, but it is generally not meant to be your only source of income in retirement. On average, Social Security will replace about 40% of your annual preretirement earnings, according to the Social Security Administration.

SoFi

While many people we polled (41%) are aware of this, a sizable percentage (31%) are counting on Social Security as their main source of income in retirement. On the flip side, a full 16% aren’t counting on Social Security at all.

Challenges and concerns

Getting to the finish line with retirement isn’t always a straight course. Our survey reveals what Americans are most concerned about when mapping out their financial future.

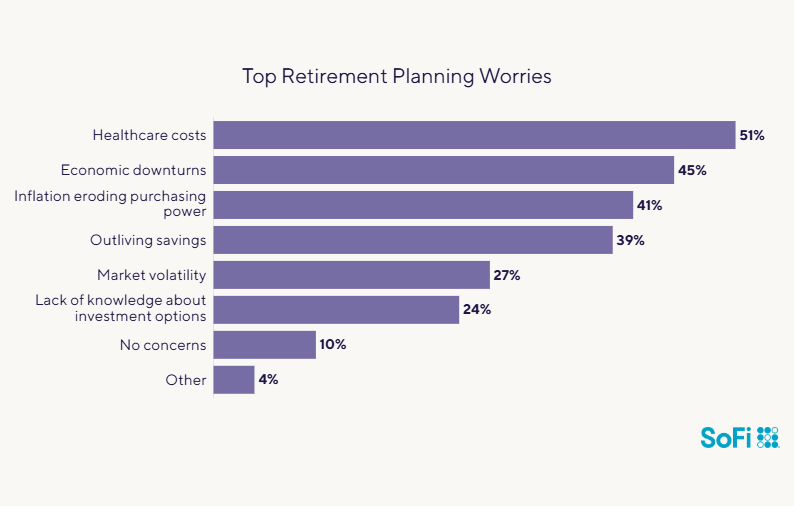

1 in 2 are worried about health care eating up retirement savings

Rising health care costs can test the strength of your retirement plan, and roughly half of people we polled cite it as their number one concern. Forty-nine percent plan to use Medicare and supplemental insurance to manage health care expenses in retirement, while 27% are putting funds into a health savings account to help cover future health care expenses.

After health care, respondents said their chief worries were (in order of importance): economic downturns, inflation, and outliving their retirement savings. Just 10% say they have no concerns about their retirement savings.

SoFi

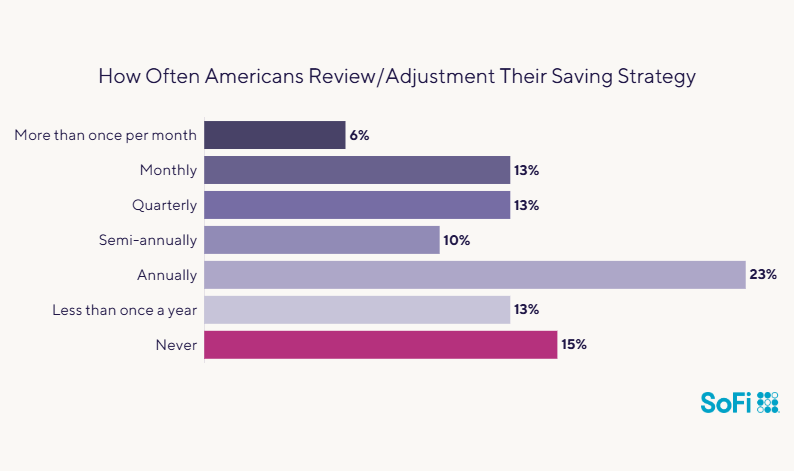

1 in 2 review their savings strategies at least annually

Financial advisors generally recommend reviewing your retirement savings accounts and overall plan at least once each year to monitor your progress and address any concerns.

The good news is that more than half of our survey participants (55%) do that or more: 23% check in once a year; 13% do quarterly reviews, and 19% check in once a month or more. But there is some room for improvement: 15% of our survey respondents admit to taking a head-in-the-sand approach and never review or adjust their retirement plan.

SoFi

The takeaway

The results of SoFi’s 2024 Retirement Survey suggest that most Americans are getting a relatively early start on saving for retirement and feel fairly confident about reaching their goals. However, our data also highlights some weak spots: Many workers aren’t putting away enough of each paycheck into savings, don’t have a clear idea of how much they will need to retire, and may not have enough stashed away to retire when they’d like.

About the survey

SoFi’s 2024 Retirement Survey was conducted on April 1, 2024, and included 500 U.S. adults aged 18 or over who were either currently saving for retirement, not currently saving for retirement but have in the past, or not currently saving but would like to start.

Percentages were rounded to the nearest whole number so some percentages may not add up to 100%.

This story was produced by SoFi and reviewed and distributed by Stacker.

![]()