Homebuyer survey: How Americans are budgeting, saving, and getting to the close

Homebuyer survey: How Americans are budgeting, saving, and getting to the close

The process of buying a home is thrilling … and complicated. And in today’s housing market, where home prices ascended steeply after mid-2020, would-be homeowners can sometimes feel like housing costs and interest rates are conspiring against them achieving their dream.

After hitting a historic high at the end of 2022, the median price of a home sold at the end of 2024 was $419,200, according to Federal Reserve Economic Data (FRED) compiled by the Federal Reserve Bank of St. Louis. So how are homebuyers coping with the quest? To find out, SoFi surveyed 500 U.S. adults looking to buy a home.* Roughly half of respondents (55%) were in the market for their first home, while the rest (45%) were repeat purchasers.

What SoFi learned: Finding a home that’s affordable and financing the purchase are the biggest concerns, with more than 2 in 5 buyers saying their top challenge is home prices, and over a third saying that understanding different mortgage options is a chief concern. Read on for the lowdown on what buyers are wondering about—and what they are doing to master the home-buying process.

Note: SoFi rounded percentages to the nearest whole number, so some data sets may not add up exactly to 100%.

*The survey was completed in April 2024 and was conducted using a general U.S. population data set of 500 adults 18 and older.

Key Findings

- Finding an affordable home and understanding mortgage options are the top challenges for homebuyers.

- Homebuyers are saving by cutting expenses, increasing savings, and finding additional income sources.

- Technology is widely used, with 65% using online listing platforms and 41% using online lenders.

- Professional advice is sought, with 36% consulting financial advisors and 42% seeking real estate attorney advice.

- Despite challenges, 81% of homebuyers are optimistic about buying within budget in six months.

Top home-buying challenges

The number of active home listings in the U.S. took a dive during the COVID-19 pandemic, as homeowners hunkered down, complicating the buying-a-home process further. And although the market has recovered somewhat, available listings, which numbered around 829,000 at the start of 2025 according to FRED, are still well off the more than 1,033,000 active listings recorded in December 2019. This is just one of the factors that has contributed to upward pressure on home prices in many markets.

Not surprising, then, that 42% of home-seekers say finding a home in their price range is their greatest challenge, according to SoFi’s survey. And even if they find a place to buy, 14% of shoppers are struggling with inadequate savings for a down payment.

If you’re worried you need 20% for a down payment, you might be pleasantly surprised to learn that in late 2024, the median down payment was 15%, according to data from the National Association of Realtors (NAR), and the typical down payment for first-time buyers was 8%.

In SoFi’s buying-a-home survey, among those who were challenged to come up with a down payment, 49% hadn’t explored down payment assistance programs—meaning they could be leaving money on the table.

More than 1 in 10 respondents (11%) said an insufficient credit score was their greatest home-buying challenge. The same proportion said difficulty securing a mortgage is their main concern—and, of course, the two issues are interrelated. Mortgage lenders use credit scores to help determine eligibility and home loan interest rates. Ten percent of respondents said a lack of certainty about their job and future income was making home buying difficult.

SoFi

Navigating the process of buying a home

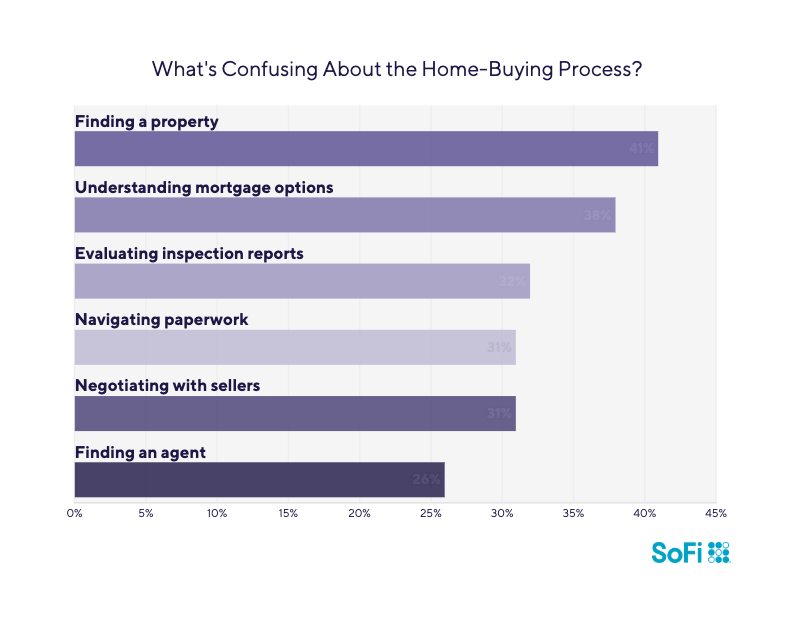

A home is the biggest purchase most people will ever make, so it’s no surprise that when asked which parts of the home-buying process were most confusing to them, the greatest number of respondents (41%) ranked finding the right property as their top issue.

Thirty-eight percent were confused by mortgage options. True, there are many different types of mortgage loans and endless jargon (APR? FHA? DTI? The acronyms alone could short-circuit a homebuyer’s brain.) Home inspection reports are confusing for 32% of people, while 31% are stymied by paperwork. Negotiating with sellers is a point of confusion for 31%, while 26% struggle with finding a real estate agent.

Technology has been a help to many home shoppers. Almost two-thirds (65%) have used an online property listing platform such as Zillow or Redfin. Online lenders have helped 41% of respondents. And 39% have used virtual or augmented reality for property viewing, with 27% using drone photography.

Virtual home tours are especially helpful to those who are buying a home without visiting it in person. Forty percent of respondents were willing to buy a home sight unseen if it meets their criteria and budget, but 39% are not (and 21% were iffy).

Among those who were willing to shop from afar, most shoppers were savvy and planned to use one or more methods to mitigate risk:

- 55% would request additional info from the seller/real estate agent.

- 49% would thoroughly research the property and neighborhood online.

- 46% would hire a local pro to inspect the property.

- 43% would explore virtual or augmented reality technology for property viewing.

- 42% would seek advice from a real estate attorney about contracts and contingencies.

Budgeting challenges and strategies

Notwithstanding concerns about high home prices and inadequate down payment savings, fully 81% of homebuyers were very or somewhat optimistic that they would be able to purchase a home within their budget in the next six months. Sadly, about one in five buyers weren’t feeling so hopeful.

SoFi

Creating a home-buying budget

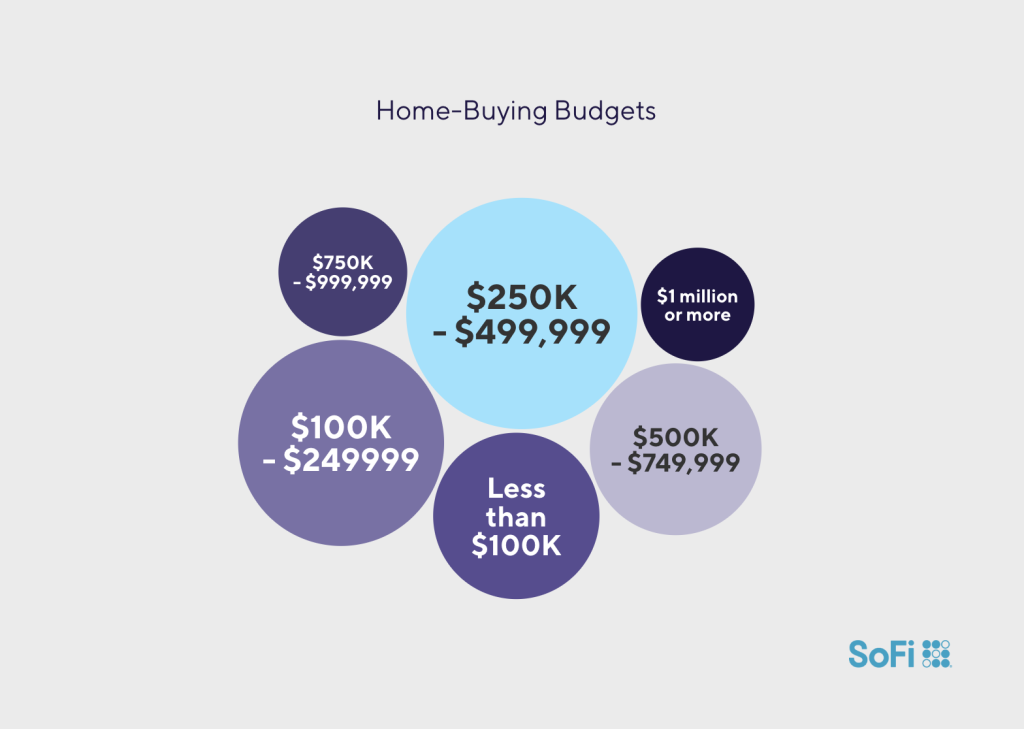

How much do homebuyers plan to spend on their new abode? With home prices already averaging over $400,000 and forecast to continue to rise moderately in 2025, more than 1 in 4 survey respondents (29%) were budgeting between $250,000 and $499,999. Fifteen percent of survey takers were looking for a bargain, planning less than $100,000. Another 23% thought they would spend between $100,000 and $249,999. A quarter of shoppers thought they would spend between $500,000 and $999,999, with 7% budgeting more than $1 million.

Interestingly, more than half of respondents whose home budget was $500K or higher have a household income of less than $100,000 per year. Some of these people could be relying on the sale of a first home to fund a second home and may even make a cash purchase. For the rest, an annual income of $100,000 typically equates to a home-buying budget in the neighborhood of $300,000.

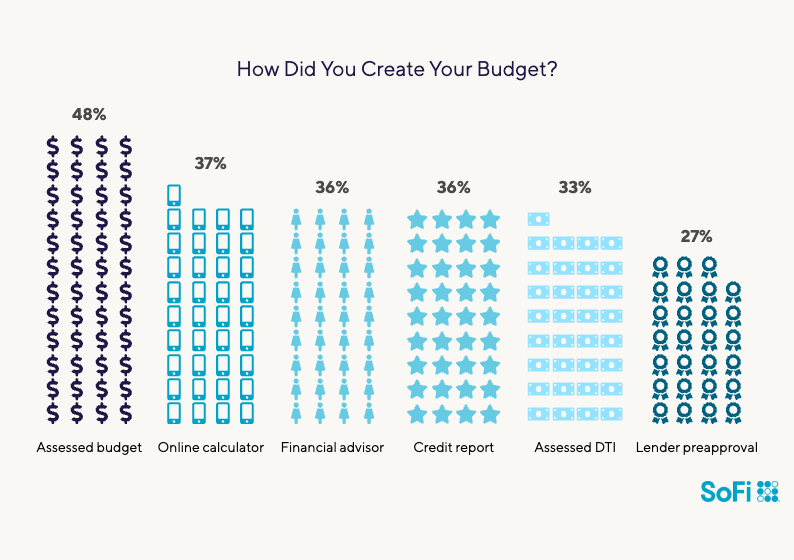

Would-be homeowners were using several methods to establish their budget. Forty-eight percent were assessing their current budget, while 37% used an online home affordability calculator. Consulting a financial advisor was also popular: 36% of people used this method. Reviewing credit scores and reports was a popular step for 36% as well. A third of shoppers (33%) assessed their debt-to-income (DTI) ratio. Twenty-seven percent got preapproved by a lender as a way of determining their budget.

SoFi

Down payments: Doing the math

The largest up-front expense associated with buying a home is usually the down payment. Here’s what shoppers were planning to spend.

- 7% of respondents were exploring zero-down-payment options.

- 10% planned to put down less than 5%.

- 19% planned to put down 6%-10%.

- 30% planned to put down 11%-20%.

- 23% planned to put down 21% or more.

- 10% of respondents weren’t sure how much they would put down.

Buying a home with a small down payment is possible with planning, and some government-backed loans, such as VA loans (backed by the U.S. Department of Veterans Affairs), don’t require a down payment. Lenders may also offer a low-down-payment option for qualified first-time homebuyers.

SoFi

Money-saving tips from homebuyers

An overwhelming majority of homebuyers—92%—have made changes in their money habits in order to save money for their home purchase. About half (49%) have trimmed nonessential expenditures and almost the same number (45%) have increased contributions to their savings. A significant number (41%) have found a side hustle to earn more income, while 26% have downsized their current living situation. About one-fourth have sought help from family or friends.

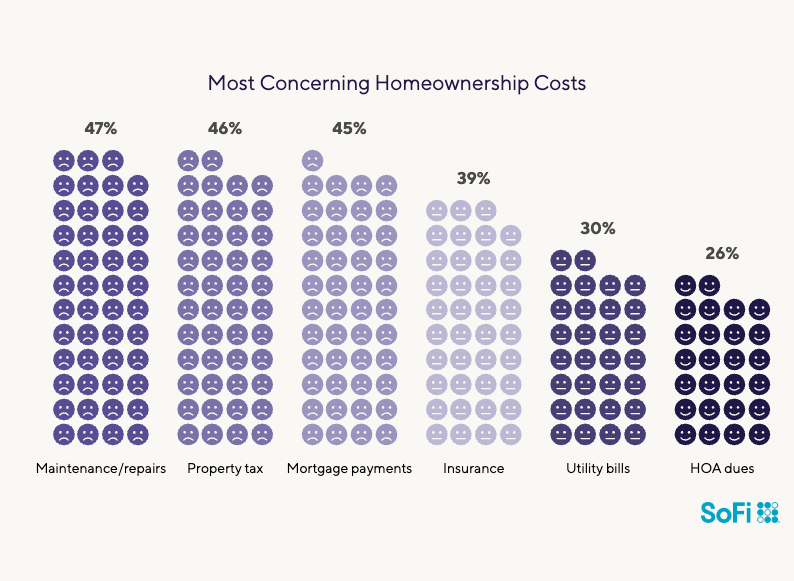

The survey suggests that buyers will continue to employ saving strategies after they close on a property, as ongoing homeownership costs were a significant concern for many respondents. Top worries included maintenance and repairs (a concern for 47%), followed by property taxes (46%), making mortgage payments (45%), affording home insurance (39%), and covering utilities costs (30%). One in four people said homeowners association costs were a concern. In fact, about 30% of U.S. housing stock is in a community governed by an HOA, according to NAR.

Choosing a lender

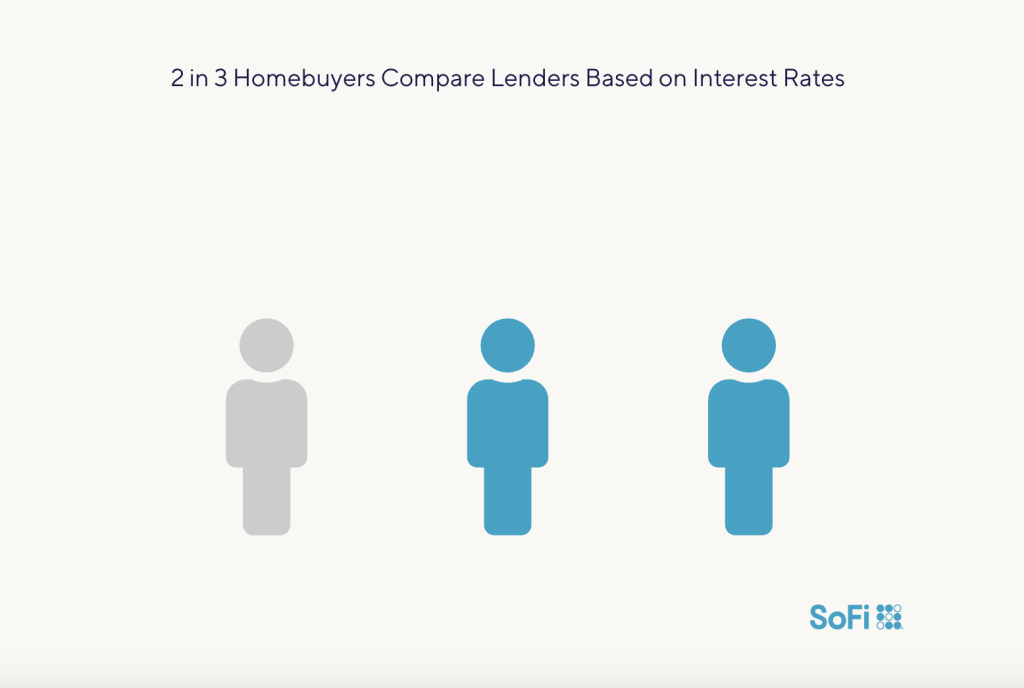

As homebuyers save money and search for a property, they’re also carefully weighing the second most critical decision in the home-buying process: selecting a lender for their mortgage loan. Roughly 1 in 4 homebuyers is paying all-cash for their purchase, an all-time high, according to the NAR. But among those who must borrow, SoFi’s survey found that interest rates were the top factor when comparing mortgage lenders. They were most important to 64% of respondents. Half of survey-takers said closing costs were a key factor, while 48% had their eye on closing costs when comparing lenders. Special programs and incentives were an important comparison point for 40%. Reputation and customer satisfaction were important to 39% of buyers.

SoFi

Getting to the loan approval

Just over half of survey respondents (53%) had completed a full loan application in their current home-buying process. One in 4 (26%) had applied for a conventional loan, while slightly more (28%) had applied for an FHA loan, backed by the Federal Housing Administration. (Use of FHA loans by first-time homebuyers has declined significantly, from 55% in 2009 to 24% in 2024 according to NAR.)

Twenty-three percent had applied for a loan backed by the United States Department of Agriculture (USDA), while 12% had applied for a VA loan. Some, of course, had applied for more than one type of loan, and a small percentage (5%) applied for a type of financing not listed here.

Awareness of government-backed loan options was fairly strong, with almost half of homebuyers (49%) having heard of FHA loans, 41% being aware of USDA loans, and 38% having some knowledge of VA loans. Almost half (49%) were also aware of rent-to-own agreements, a less common form of financing. About a third (34%) were aware of interest-only mortgages.

The takeaway

Today’s homebuyers are most concerned with the financial aspects of the home-buying process, with finding an affordable property, saving for the home purchase, and comparing lenders’ interest rates topping their list of important factors. The good news is that, despite high home prices and stubborn interest rates, more than 4 in 5 buyers were optimistic about completing the home-buying process and making their purchase within the next six months.

FAQ

What is the process of buying a home?

The process of buying a home starts with determining what you can afford and planning for a down payment, if you can afford one. Seeking mortgage preapproval can help you understand how much you might be able to borrow. Once you have a sense of your budget, working with a real estate agent can help you locate properties. If you find your sweet spot, you’ll make an offer, finalize your home loan, negotiate with the seller and, ultimately, close the deal.

What are the 5 stages of buying a home?

The five stages of buying a home are planning (setting your budget, determining your down payment), preapproval (getting preapproved for financing), searching (you’ll find a real estate agent and identify a property), negotiating (you’ll get an inspection and go back and forth with the seller), and finalizing (you’ll solidify your financing and go to the closing table).

Can I move in on closing day?

You can move in immediately once you close on a house, as long as your contract doesn’t stipulate a different occupancy date.

What are closing cost fees?

Closing costs are fees paid to the team that helps get you into your new home. These can include fees for the appraiser and title company, lender fees, and more. As a general rule, closing costs average 3% to 6% of your mortgage loan principal.

What are the 4 C’s when buying a home?

The 4 C’s of home buying are the things that a lender will consider when deciding whether to approve your home loan application and determining what interest rate and terms you qualify for. They are Capacity (ability to repay the loan), Capital (funds available to you in the form of savings and other assets), Collateral (the value of the property that will be the collateral for the loan), and Credit (your credit scores and history).

This story was produced by SoFi and reviewed and distributed by Stacker.

![]()