The consequences of an unreported fender bender

Siarhei Kuranets // Shutterstock

A fender bender can feel like a minor inconvenience, a brief, stressful disruption quickly resolved with a handshake and an agreement to “keep the insurance companies out of it.” Drivers often make this snap decision to avoid the immediate hassle of filing a claim or the feared increase in their car insurance rates.

However, choosing to handle a car accident privately, regardless of how minor it appears at the scene, is a financially and legally dangerous gamble. That small dent or scratch, which seems resolvable with a few hundred dollars in cash, can quickly escalate into a catastrophic liability claim, denied coverage, or state-level legal penalties, including driver’s license suspension.

Ignoring an incident, even a seemingly trivial one, is an action that puts you in violation of your insurance contract and leaves you financially exposed. CheapInsurance.com breaks down the serious and often-overlooked ramifications of keeping a car accident a secret and provides the essential information you need to protect yourself from unnecessary risk.

What Happens if I Don’t Report a Minor Car Accident to My Insurance Company?

The primary reason most drivers opt not to report a minor accident is the assumption that it will be quicker and cheaper to handle the damages privately. However, this decision immediately puts you in violation of your insurance contract and leaves you completely exposed to financial disaster.

An auto insurance policy is a contract, and nearly every policy contains a clause requiring the insured to provide “prompt notification” of any incident that could reasonably lead to a claim. By not reporting the fender bender, you breach this fundamental term.

The consequences of this breach are severe and immediate:

- Claim Denial: If the other driver later changes their mind, or discovers a delayed injury, and files a claim against you, your insurance company can invoke the lack of prompt notification to deny coverage for the entire claim. This means you would be personally responsible for all property damage repairs, medical bills, and legal defense costs. The small amount you saved on a potential premium increase could balloon into tens of thousands of dollars in out-of-pocket expenses.

- Impaired Investigation: When an insurer is notified late, they cannot properly investigate the scene, interview witnesses, or assess the damage while the evidence is fresh. This lack of ability to defend you is what “prejudices” their case and provides the grounds for claim denial.

- Policy Cancellation: Repeated failure to report incidents, even minor ones, can be viewed as a pattern of contract violation, leading to the cancellation or non-renewal of your policy. Finding new insurance after a cancellation for non-cooperation can be extremely difficult and expensive.

Penalties For Failing to Reporting to the DMV

- Driver’s License Suspension: The state may issue an automatic suspension or revocation of driving privileges. This penalty is triggered when an accident that meets the mandatory reporting criteria is discovered by the DMV without the required report from the driver.

- Mandatory SR-22 Filing: A license suspension for failing to comply with reporting rules frequently necessitates the filing of an SR-22 Certificate of Financial Responsibility. This places the driver into the high-risk insurance category, leading to significantly increased premiums for a period of several years.

- Fines and Misdemeanor Charges: Depending on the jurisdiction and severity of the unreported accident, the offense may be classified as a violation, infraction, or a misdemeanor criminal charge, resulting in monetary fines and points on the driving record.

Beyond your personal insurer, you may have a legal obligation to report the accident to the state’s Department of Motor Vehicles (DMV) or equivalent agency. In many jurisdictions, any accident resulting in property damage over a certain threshold (often $1,000) or causing any injury, regardless of fault, must be reported to the state within a defined timeframe. Failure to comply with this specific legal requirement can lead to far greater penalties than an insurance claim, including fines, driver’s license suspension, and the mandatory filing of an SR-22 certificate of financial responsibility. SR-22 insurance is essentially a high-risk insurance filing that drastically increases your insurance rates for a period of years.

CheapInsurance.com

(Data compiled and estimated from analysis of national average premium increases, typical personal injury defense costs, state-mandated SR-22 insurance surcharges, and liability judgments.)

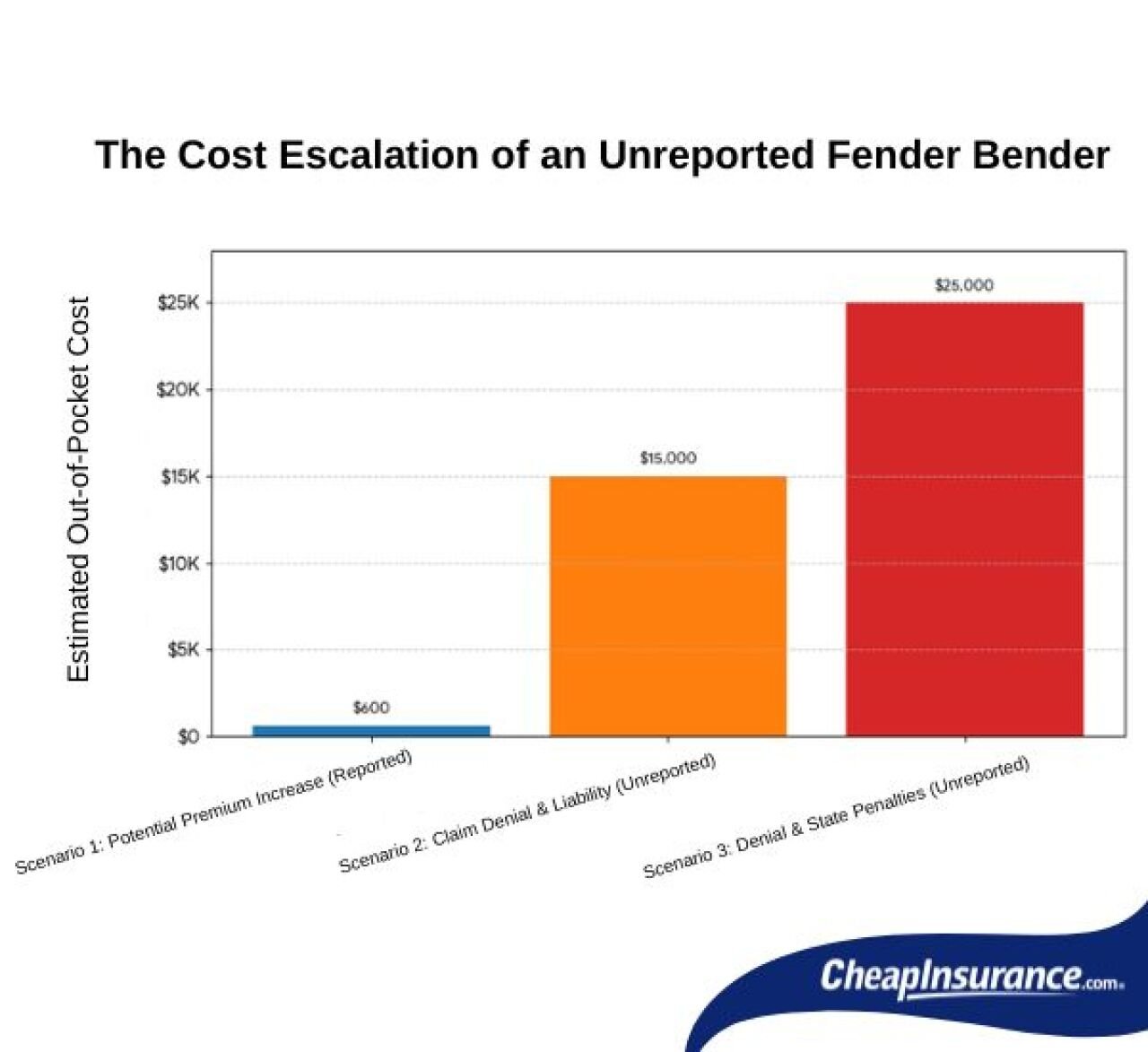

The Visual: Cost Escalation of an Unreported Fender Bender

This chart compares the maximum financial impact of three scenarios:

- Scenario 1 (Reported): The potential increased cost of your insurance premium over three years for a minor, at-fault incident.

- Scenario 2 (Unreported – Claim Denial): The out-of-pocket cost if your insurance denies coverage for a moderate personal injury lawsuit (covering legal fees and liability payment).

- Scenario 3 (Unreported – Denial + State Penalties): The cost of denial plus the extra expense of three years of high-risk SR-22 insurance mandated by the state.

Will Reporting a Small Accident Always Raise My Insurance Rates?

This question is the core of the driver’s hesitation, and the answer is no, reporting an accident does not automatically raise your insurance rates. While it is true that filing a claim can lead to an increase, the relationship between reporting an incident and your premium is more nuanced and depends on several key factors:

- Fault Determination: The most significant factor is who was determined to be at fault. If you are found to be zero-percent at fault, reporting the claim is highly unlikely to affect your premium, as it is a non-chargeable incident. You are simply notifying your company for protection.

- Claim Payout: Insurance companies are primarily concerned with the financial risk you pose. If a claim is reported but ultimately results in no payout (e.g., the damage falls below the deductible, or the other party drops the claim), it often has minimal or no impact on your rates.

- Accident Forgiveness: Many insurers offer “accident forgiveness” programs for loyal, long-time customers, meaning your first at-fault accident will not result in a premium increase.

- Claim Type: Non-fault claims, such as comprehensive claims (like hail or theft), or non-chargeable accidents (like being rear-ended by a driver who was cited), are generally viewed differently than at-fault collision claims.

The reality is that an insurer will eventually find out about a non-reported accident if the other driver files a claim. At that point, not only might your rates increase due to a found-at-fault claim, but you will also face the penalty of contract breach and potential claim denial. It is far better to report the incident, secure your full legal protection, and face the minimal risk of a rate adjustment, than to risk total financial ruin.

How Does an Unreported Car Accident Affect a Vehicle’s Future Resale Value?

An often-overlooked financial consequence of an unreported accident relates directly to your car’s market worth, a concept known as diminished value.

In the modern used car market, a vehicle’s history is rigorously tracked through services like CarFax and AutoCheck. These services primarily rely on two sources of data: collision repair shops and insurance claims. If a fender bender is minor and is handled entirely outside of the insurance and official systems, the repair work may not generate a formal record.

However, if you and the other driver agree to a private cash settlement, and the other driver uses that money for repairs at a body shop that does report to a national database, the accident is documented on the vehicle’s history report. If you later try to sell your vehicle, a potential buyer seeing this report will notice the damage history. Since there is no corresponding police or insurance report, the damage history is vague, forcing the buyer to assume the worst.

In this scenario:

- Loss of Negotiating Power: You, as the seller, have no official paperwork (a police report or insurance file) to explain the damage was truly minor.

- Reduced Price: The buyer will demand a significant reduction in the vehicle’s resale value, the diminished value, to compensate for the undocumented accident history.

Conversely, if you report the accident and the insurance company manages the repair, a formal, detailed claim file exists. This file can be used to prove to a future buyer that the damage was professionally repaired, limited in scope, and that the appropriate financial responsibility was met, which helps to mitigate the impact of the accident on your vehicle’s eventual resale price. By failing to report, you essentially leave a vague, negative mark on your vehicle’s title history that you have no verifiable paperwork to refute.

What is the Legal Deadline for Reporting an Accident and Why is it Important?

The legal deadline for reporting an accident has two separate components, both of which are crucial: the requirement from your insurance company and the mandate from the state DMV.

1. Insurance Company Deadline: Most auto insurance policies require you to report an accident “promptly” or “as soon as reasonably practicable.” While this term is vague, in practice, it generally means within 24 to 72 hours. Sticking to this immediate timeframe is essential because it eliminates your insurer’s ability to claim you violated the contract due to late reporting, thus ensuring your full coverage and legal defense are secured from the outset.

2. State/DMV Legal Deadline: State laws govern the maximum time you have to file a state required accident report with the relevant state authority (often the DMV or State Police). While these rules vary, it is a common legal requirement across many states that an accident resulting in property damage over the statutory limit (e.g., $1,000) or any injury/death must be reported to the DMV within 30 days of the incident.

Importance of the 30-Day Limit:

- License Protection: Failing to meet this legal, 30-day deadline can result in a driver’s license suspension.

- SR-22 Mandate: As noted earlier, if you fail to report an accident that legally requires one (such as those involving damage over $1,000) and the state becomes aware of it through the other party, you may be issued a demand to file an SR-22 Certificate of Financial Responsibility. This is a specific penalty often associated with uninsured or reckless driving and is a significantly greater financial burden than any insurance premium increase.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.

![]()