What homeowners must know about their insurance quotes as the year ends

David Gyung // Shutterstock

For many, this is a moment of dread, a time when a seemingly simple piece of paper reveals a price hike that feels like a punch to the wallet. But what if someone told you the end of the year isn’t just about eggnog and New Year’s resolutions? It’s a prime, strategic window to seize control of your policy, challenge those rising costs, and ensure your most valuable asset is protected. The insurance world is complex, but understanding the forces at play, especially as the year concludes, can turn you from a passive policyholder into an empowered consumer.

This isn’t about scare tactics; it’s about smart planning. Cheap Insurance is going to dive deep into the forces that shape your home insurance quote, reveal the money-saving levers you can pull, and give you the knowledge to make your renewal conversation a productive one. Let’s make this year-end review the one that finally pays off.

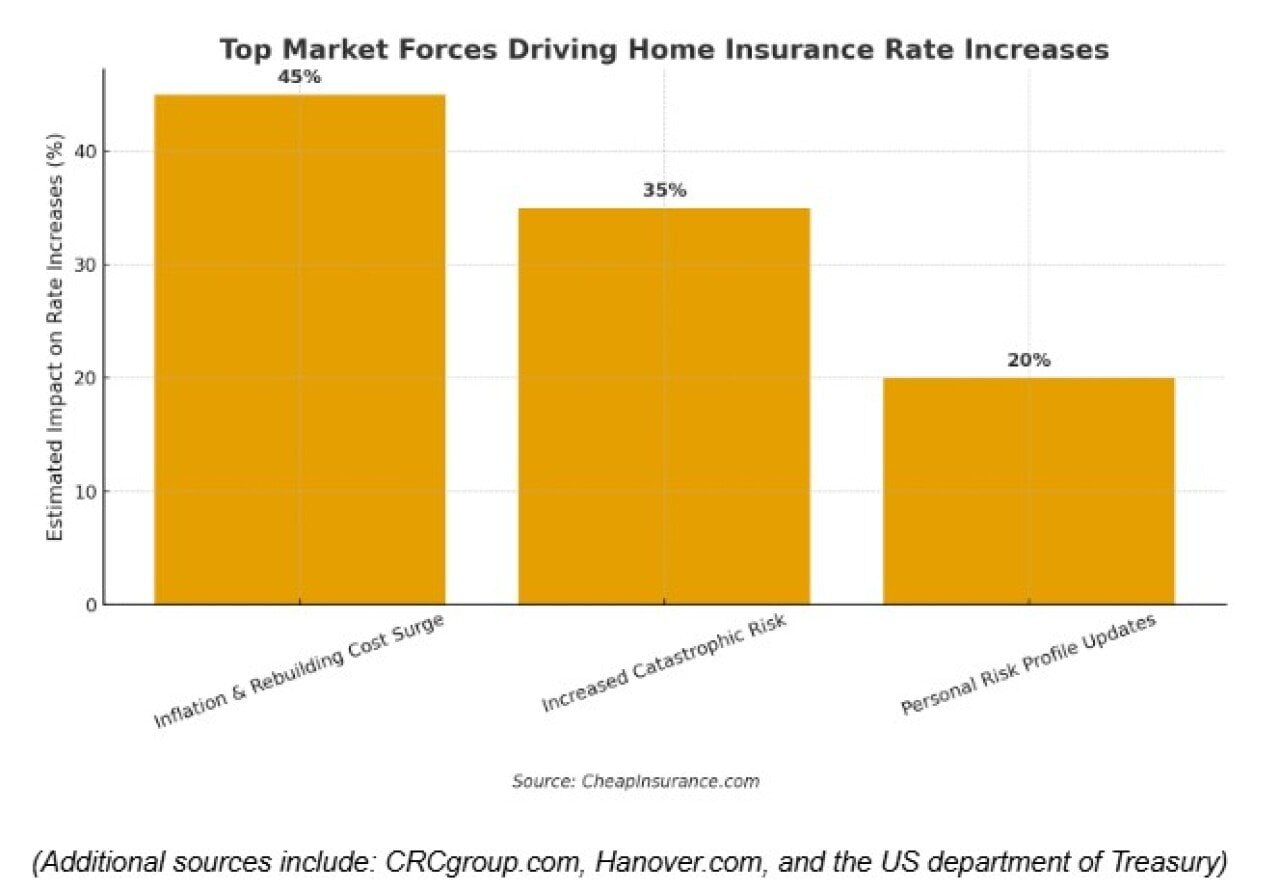

The Three Market Forces Driving Home Insurance Rates

Before discussing savings, you need to understand why that number keeps climbing. Your quote is not a random draw; it’s a cold, hard calculation based on three major, often accelerating, market forces that tend to culminate around renewal cycles.

1. The Inflation and Rebuilding Cost Surge

This is the biggest factor right now, and one that is amplified as the year closes and new construction cost data is finalized. Insurance isn’t based on your home’s market value (what you could sell it for, including the land); it’s based on the replacement cost, the cost of materials and labor to rebuild your home from the foundation up.

- Materials volatility: Construction material prices (lumber, concrete, copper) have seen massive volatility. If the cost of rebuilding your home has increased by, say, 15% this year, your insurer must raise your dwelling coverage limit to avoid leaving you dangerously underinsured in a total loss scenario. A higher coverage limit means a higher home insurance rate.

- Labor scarcity: A shortage of skilled construction labor, especially after major weather events, drives up hourly rates, further inflating the total replacement cost calculation.

Check your dwelling coverage limit. Has your insurer automatically increased it? If so, it’s likely a necessary inflation adjustment, but you should verify it aligns with local rebuilding costs, not inflated market value.

2. Increased Catastrophic Risk and Climate Volatility

The data doesn’t lie: Major weather events, wildfires, intense hail, severe storms, and flooding, are increasing in frequency and severity. Insurers are in the business of assessing and pricing risk, and if your geographic area has seen an uptick in claims (even if you haven’t filed one yourself), the collective risk for the entire region goes up.

- Regional re-rating: Insurers analyze year-end data on localized weather patterns and historical home insurance claims. If your ZIP code has become statistically riskier due to recent storm activity, expect your insurance quotes to reflect that change.

- Deductible changes: Policies in high-risk zones may see the introduction of separate, higher percentage-based deductibles for specific perils like wind, hail, or hurricanes, changing your out-of-pocket exposure.

CheapInsurance.com

CheapInsurance.com used data from CRCgroup.com, Hanover.com, and the Department of the Treasury to create the chart above.

3. Personal Risk Profile Updates

The end of the year is when the most up-to-date data on the policyholder is available. This is factored into your new home insurance quote. This includes things you might not even realize your insurer tracks.

- Claims history (the Comprehensive Loss Underwriting Exchange report): Filing even a small claim in the last five years can significantly impact your perceived risk, sometimes raising your insurance rate by 20% or more upon renewal.

- Credit-based insurance score: In most states, your financial behavior (your credit-based insurance score, which is a different model from your standard FICO score) is a key rating factor. If your credit has dipped in the last 12 months, your insurance rate could rise, as data often links lower credit scores to a higher propensity for filing claims.

Your End-of-Year Action Plan for Affordable Home Insurance Quotes

Now that you know the what, let’s get to the how. Use the end-of-year review cycle to your advantage with these proactive steps.

Step 1: The Pre-Renewal Policy Deep Dive

Don’t wait for the renewal notice to land. Review your existing policy now and look for outdated information or opportunities.

- Audit your personal property: Did you sell a high-value item, like an expensive art piece or jewelry, that was covered by a specific endorsement? Drop the endorsement. Conversely, did you purchase a new high-value item? If so, you may need to add an endorsement (often called a “rider”). Don’t wait for a loss to discover you’re undercovered.

- Review your deductible: The single easiest way to lower your home insurance is to increase your deductible. If you’re currently at $500, could you comfortably afford $1,000 or even $2,500 out-of-pocket if a major event occurred? A higher deductible signals to the insurer that you’re willing to absorb minor costs, reducing your premium by 10% to 25%.

- Check for errors: Insurance companies are not infallible. Verify your home’s basic information: square footage, year built, roof age, and construction materials. A simple typo can put you in a higher-risk category.

Step 2: Leverage Safety and Smart Home Upgrades

This is where your investments pay off. Did you make improvements this year? Don’t assume your insurer knows.

- The big three system updates: Insurance companies love updated roofs, plumbing, and electrical systems. A roof replacement or updating old knob-and-tube wiring to modern breakers significantly reduces fire and water risk. Call your agent and provide the completion dates for these major projects.

- Security and smart home discounts: The rise of smart home technology is a huge discount lever. Ask about discounts for professionally monitored security systems, smart smoke/carbon monoxide detectors, or, the new gold standard, automatic water shut-off valves. These devices mitigate claims before they become catastrophic and can earn you significant savings.

Document all home improvements, especially system upgrades (roof, electrical, plumbing), and actively inform your insurer and all quoting companies to secure potential discounts.

Step 3: The End-of-Year Shop-Around

You are not married to your current insurance provider. The end of the year, before the policy rolls over, is the absolute best time to shop.

- Bundle and save: The multipolicy discount, bundling home insurance and auto insurance policies, is often the single biggest discount available, sometimes saving you up to 30% on your total insurance bill. If you’ve never looked at bundling, now is the time to get a quote from a single carrier for both.

- Check the competition: Rates for the exact same coverage can vary wildly between providers. A company that was uncompetitive last year might be offering lower rates now. Don’t waste time on just one homeowners insurance quote; aim for three to four independent quotes to establish your true market value.

- Dig for lesser-known discounts: When talking to an agent, ask about possible discounts. For example, a nonsmoker discount, a paid-in-full discount (paying the annual premium upfront), a new home buyer discount, or even a loyal customer discount.

Getting home insurance quotes at the end of the year isn’t just an expense; it’s an annual financial audit and a promise of protection. Understanding the external pressures of inflation and climate risk, proactively reviewing your policy details, and aggressively shopping the market ensures that you are not just taking a price but instead negotiating the best possible value. A little effort now can lead to a lot of savings and, more importantly, peace of mind knowing your most important investment is properly covered for the year ahead.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.

![]()