Real Borrowers, Real Reasons survey: Who is taking out personal loans and why

fizkes // Shutterstock

Real Borrowers, Real Reasons survey: Who is taking out personal loans and why

The past five years have presented many Americans with financial headaches of all sorts: high grocery costs, steep housing prices, job uncertainty, COVID-related setbacks, and more. To cope with busted budgets and expenses that just can’t wait, more and more households are borrowing money in the form of unsecured personal loans. As of April 2025, the average balance per consumer stood at more than $11,600, according to TransUnion.

To learn more about why people get personal loans and how those personal loans are used, in April SoFi conducted its Real Borrowers, Real Reasons survey. Participants included 1,000 adults across the country who have taken out at least one personal loan in the past five years. More than one-third of them had secured two or more during that time period.

They were asked about their loan rates and terms, how much they borrowed, what they’ve been using the money for, and their experience managing the loan payments. Read on for the intriguing results.

Key Findings

Some highlights of SoFi’s 2025 Real Borrowers, Real Reasons survey:

- 58% of people borrowed less than $10,000.

- 43% of respondents have fully paid off their loan.

- Nearly half (48%) paid off their loan within two years.

- 1 in 4 people used their personal loan for debt consolidation, the most common motive.

- 64% reported interest rates of 9% or below.

- Even so, respondents most commonly identified high interest rates as the biggest challenge to managing their loans.

Analyzing the personal loan statistics showed that people tended to borrow moderately (most took out less than $10,000) and pay their personal loans back promptly. Given the chance, the vast majority (79%) would do it all over again, since most people (65%) felt the loan left them in a better financial position.

However, 1 in 5 respondents felt their finances did not improve after the loan and, in retrospect, regret using a loan for the purpose they chose.

Survey Respondents

- More than half of the respondents were Gen Xers (30%) and Millennials (31%).

- 27% were baby boomers, and 11% members of Gen Z.

- Just over 75% identified themselves as white, with 10% identifying as Black or African American.

- Roughly 40% hail from the southern U.S., while fewer than 15% live in Western states.

- About 30% have incomes of $100,000 or more; almost 36% earn between $50,000 and $100,000.

- 6.6% had borrowed $50,000 or more.

What Was Learned: Personal Loan Statistics

Here, take a closer look at how much people borrowed, for how long, and at what interest rate, along with other key findings from the SoFi Real Borrowers, Real Reasons survey.

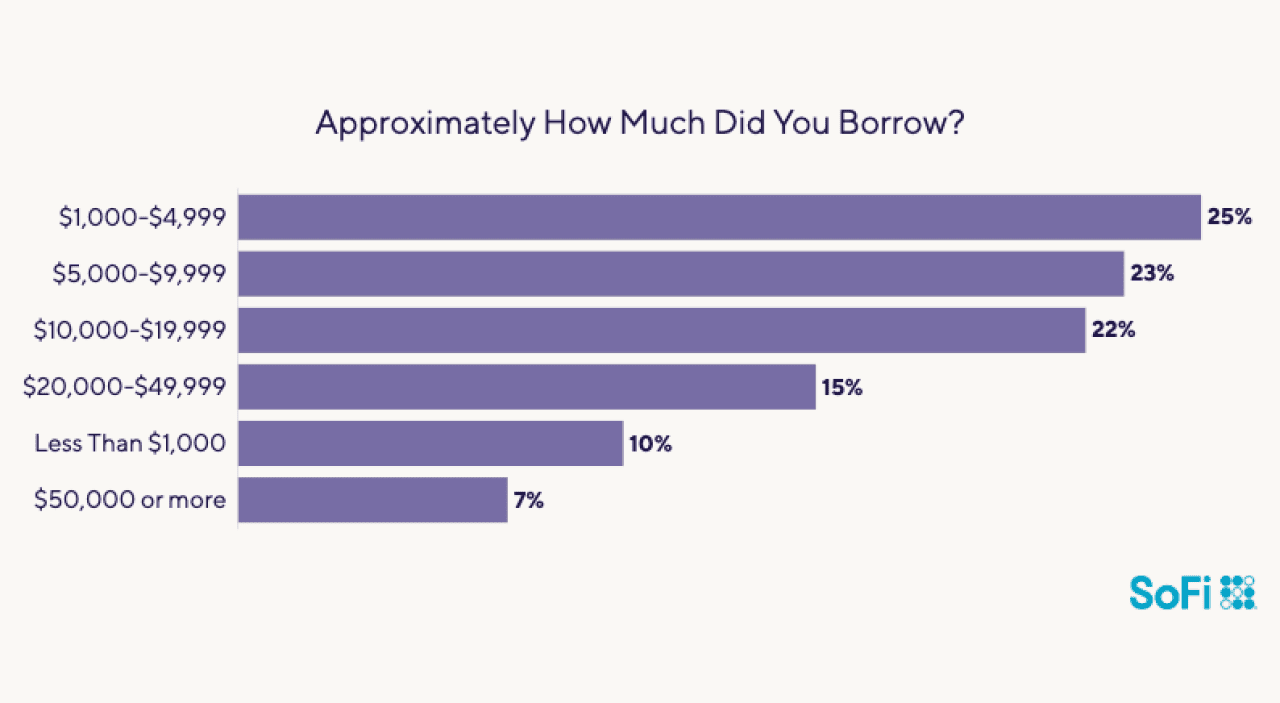

Most People Borrow Less Than $10,000

The majority (58%) of respondents took out personal loans of less than $10,000. Specifically, 23% accessed between $5,000 and $9,999, 25% borrowed between $1,000 and $4,999, and 10% secured less than $1,000. The most common use of funds by the “less than $5,000” club? Emergency expenses.

SoFi

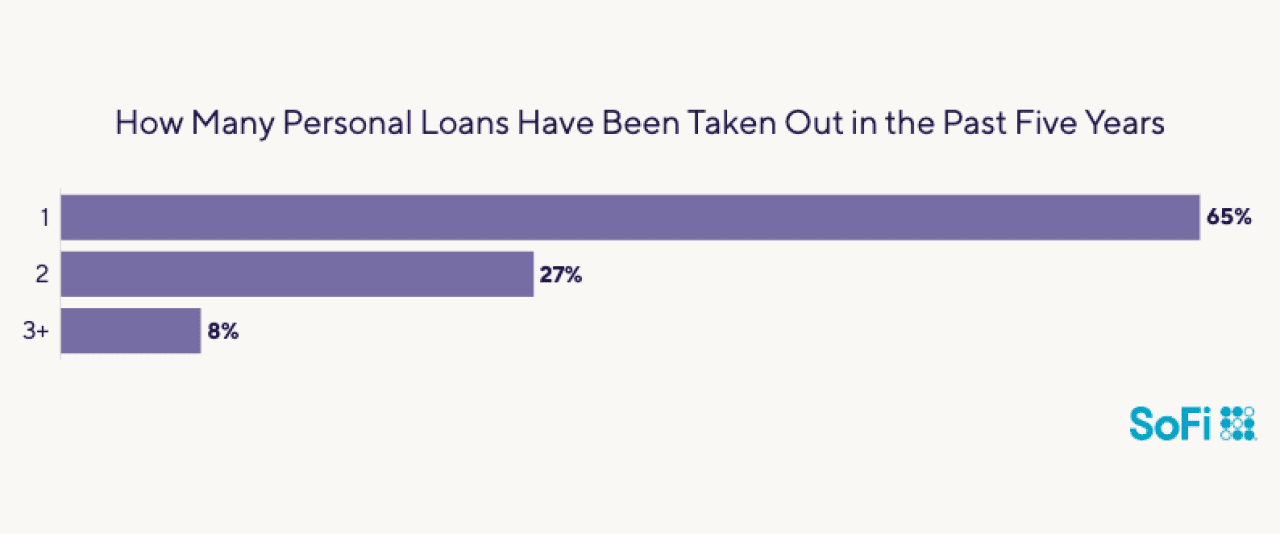

35% of Borrowers Have Multiple Personal Loans

Within the past five years, more than 1 in 3 respondents had taken out multiple personal loans, with over a quarter carrying two loans. Still, the majority (65%) limited their unsecured personal loans in the last half-decade to just one.

SoFi

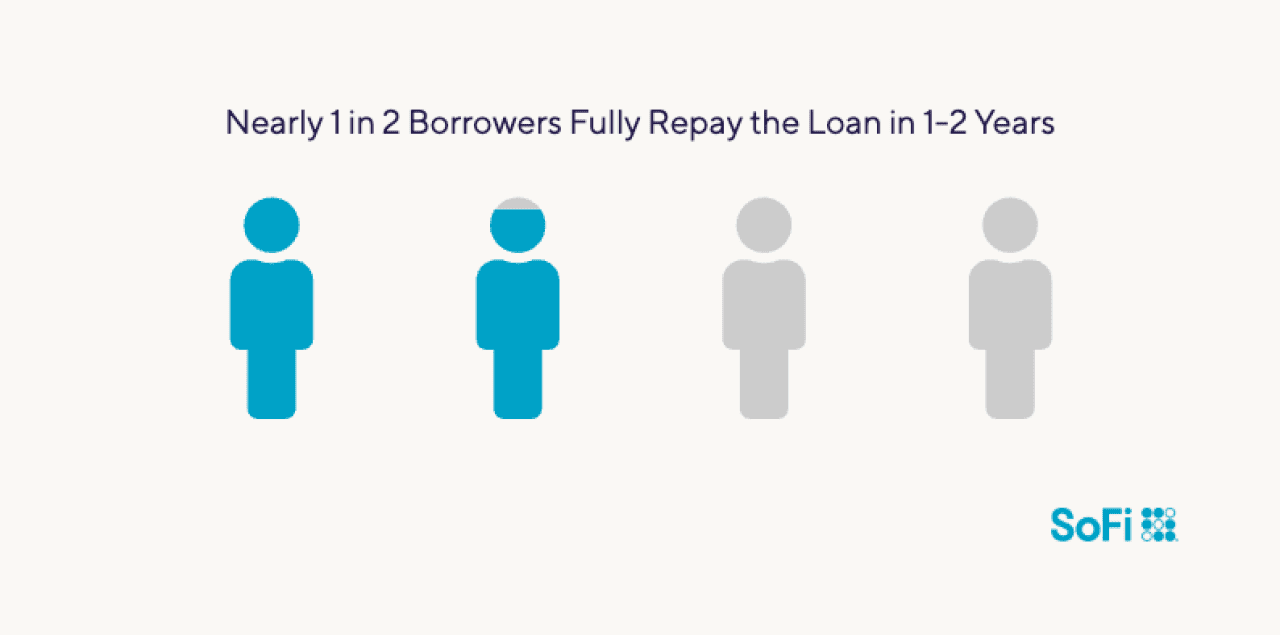

32% Repaid Their Loan Within Two Years

The amount of a personal loan usually correlates with its term length, so moderate loans are generally paid off in a few months or years. More than half of borrowers took on less than $10,000 in personal loan debt; nearly half of borrowers were able to pay off their loans within two years.

SoFi

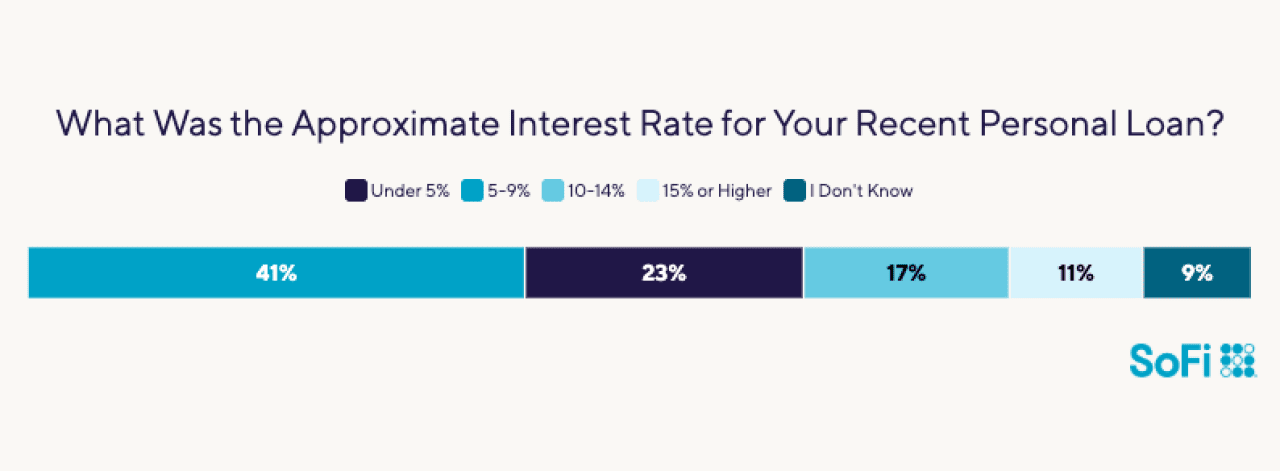

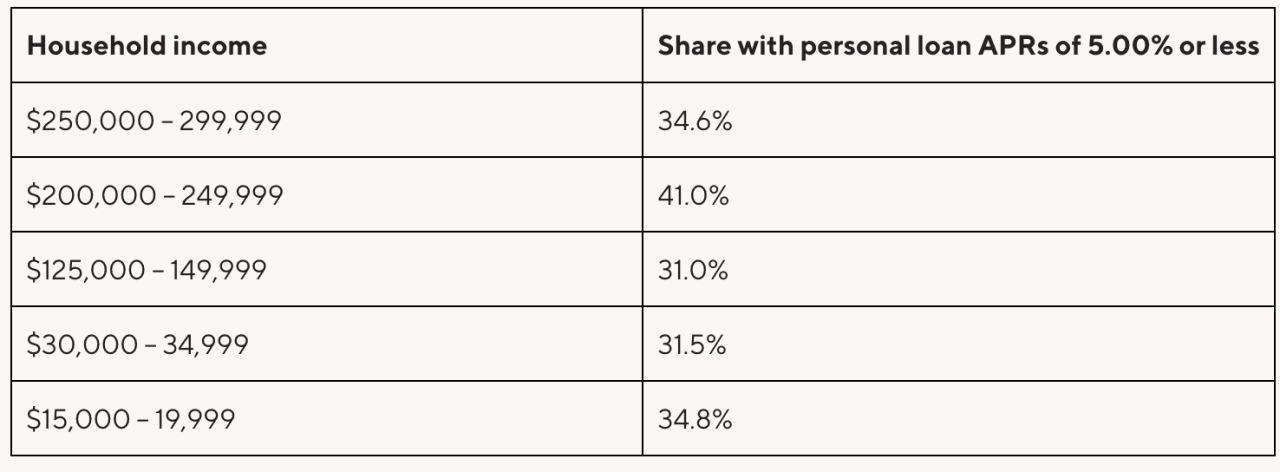

41% of Borrowers Received an Interest Rate Below 10%

More than four out of every 10 borrowers paid a rate between 5% and 9% on their loans. Almost one-quarter of respondents reported interest rates below 5%, while less than half that number are paying 15% or more.

SoFi

Usually, the people with higher incomes were the ones scoring loan rates under 5% — but not always. Almost 35% of people earning $15,000 to $19,999 reported similarly low APRs.

SoFi

53% of Borrowers Are Still Repaying Their Loan

More than half of borrowers are still in the process of paying off their most recent personal loan, compared to 43% who’ve fully paid it off.

Sizable subsets of borrowers reported that they had paid off their loans promptly or, in some cases, ahead of time. For example:

- 33% of people with one- to two-year loans were able to pay them off in 12 months or sooner.

- 30% of people with three- to four-year terms were able to pay off their loans in two years or less.

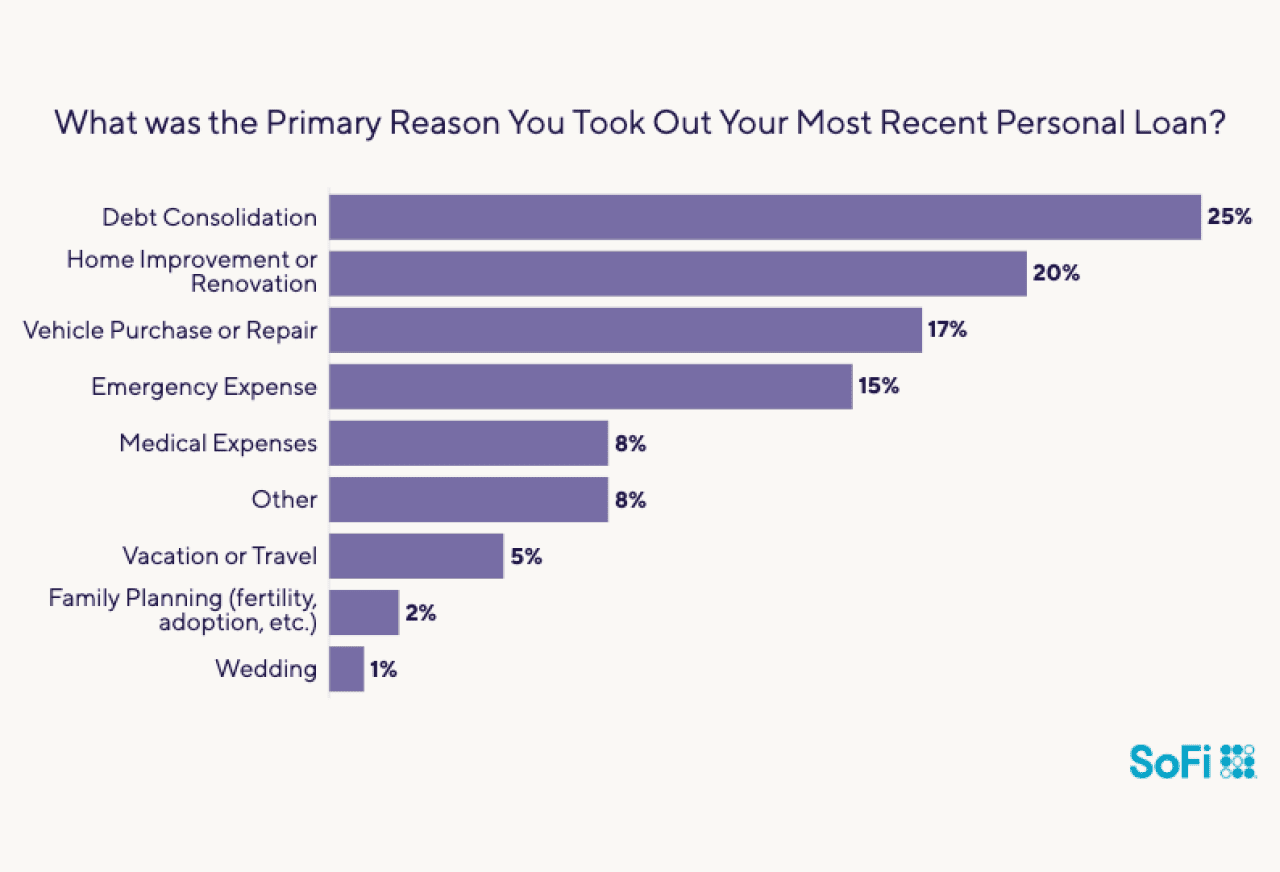

Why People Took Out Personal Loans

The uses of personal loans are many and varied, and SoFi’s survey respondents named an array of reasons for taking out personal loans. Some had big plans for the money, such as renovating their home, buying a car, traveling, or hosting a wedding.

Other borrowers had needs that they hadn’t foreseen, such as emergency expenses (say, needing a major household or car repair or being hit with a sky-high medical or dental bill).

Read on to see the specifics.

SoFi

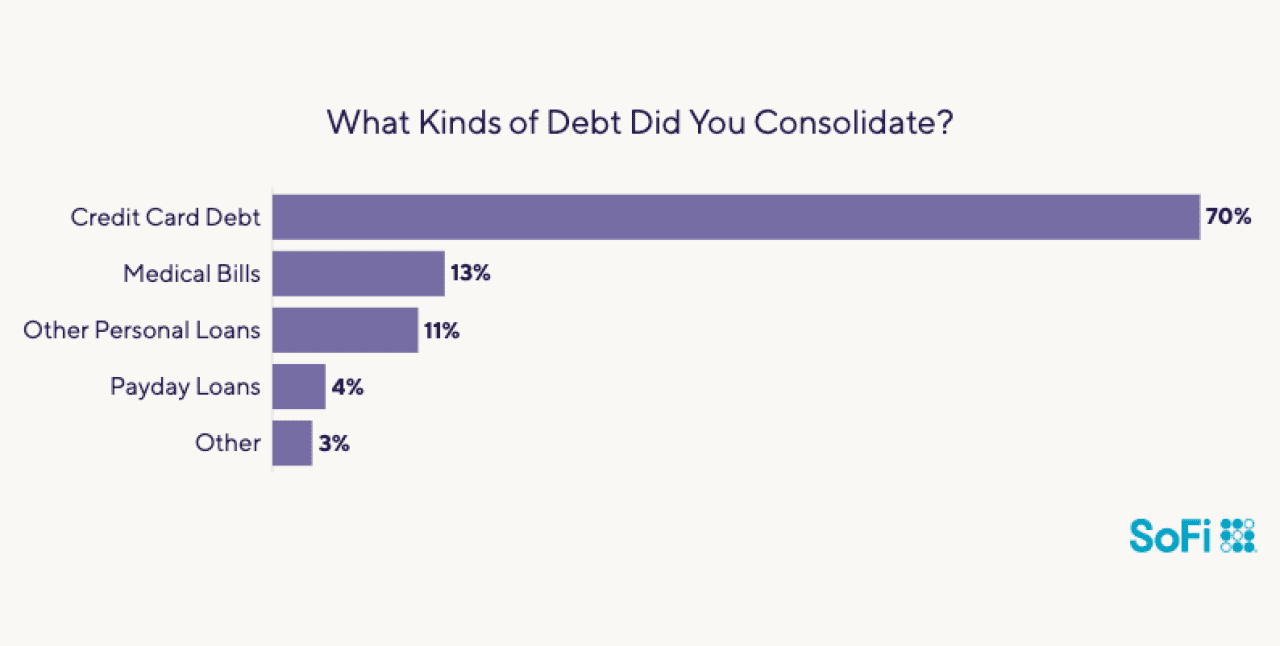

25% Used Their Loans to Consolidate Debt

Refinancing existing debt is a classic strategy for shrinking your monthly bills, and one-quarter of survey respondents cited debt consolidation as their loan’s primary purpose.

Fully 70% of that group used the money to consolidate credit card debt, a smart move given how much lower personal loan rates can be. For example, in February 2025, the average 24-month personal loan rate was 11.66%, while the average credit card APR (annual percentage rate) was 21.37%.

SoFi

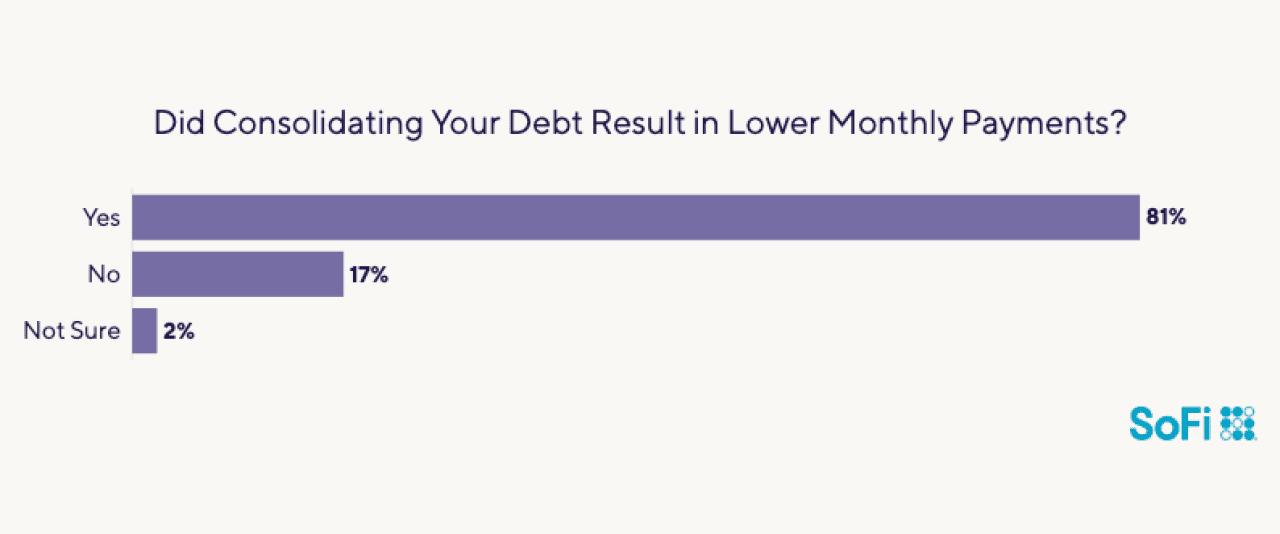

By securing a debt consolidation loan, 81% of people reported that the move lowered their monthly payments.

SoFi

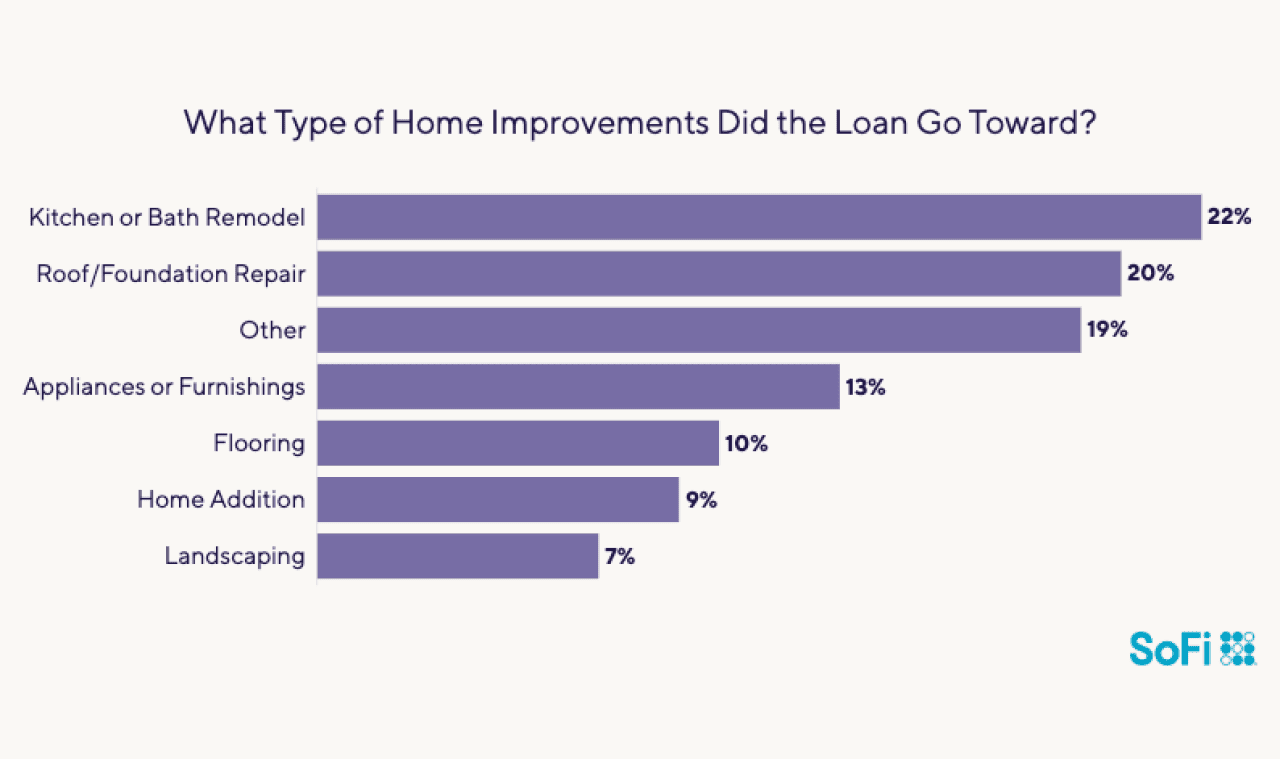

20% Put Their Personal Loan Toward Home Improvement or Renovation

One in five people said they borrowed money for home improvement or renovations. These respondents tended to take on practical projects, such as remodeling the kitchen or bath (22%) or repairing their property’s roof or foundation (20%).

Another 15% used a personal loan to consolidate debt from previous loans, including payday loans.

SoFi

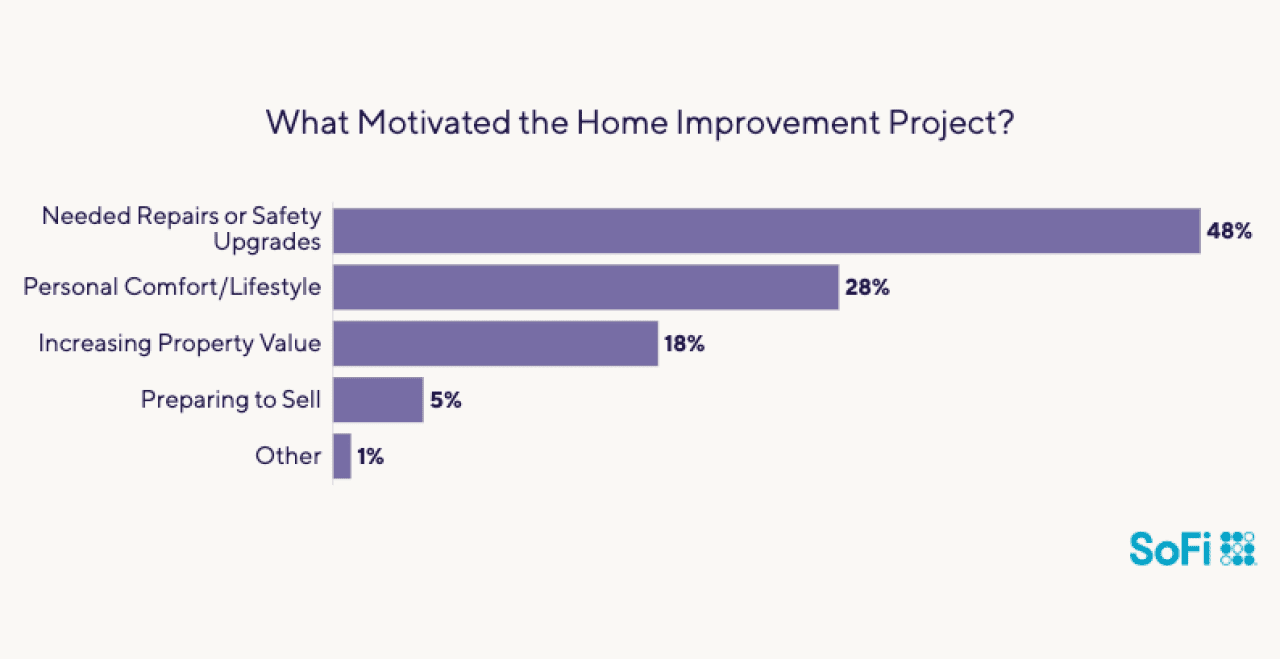

Almost half of the group (48%) said the changes were necessary repairs or safety upgrades. More than a quarter (28%) of the borrowers revamped their homes in order to reflect their personal comfort or lifestyle.

SoFi

Roughly 18% used the money to make changes that would improve their home’s property value. Fewer than 5% said the renovations were made in preparation for selling their homes, whether that involved updates or staging fees.

17% Snagged a Personal Loan to Buy or Repair a Car

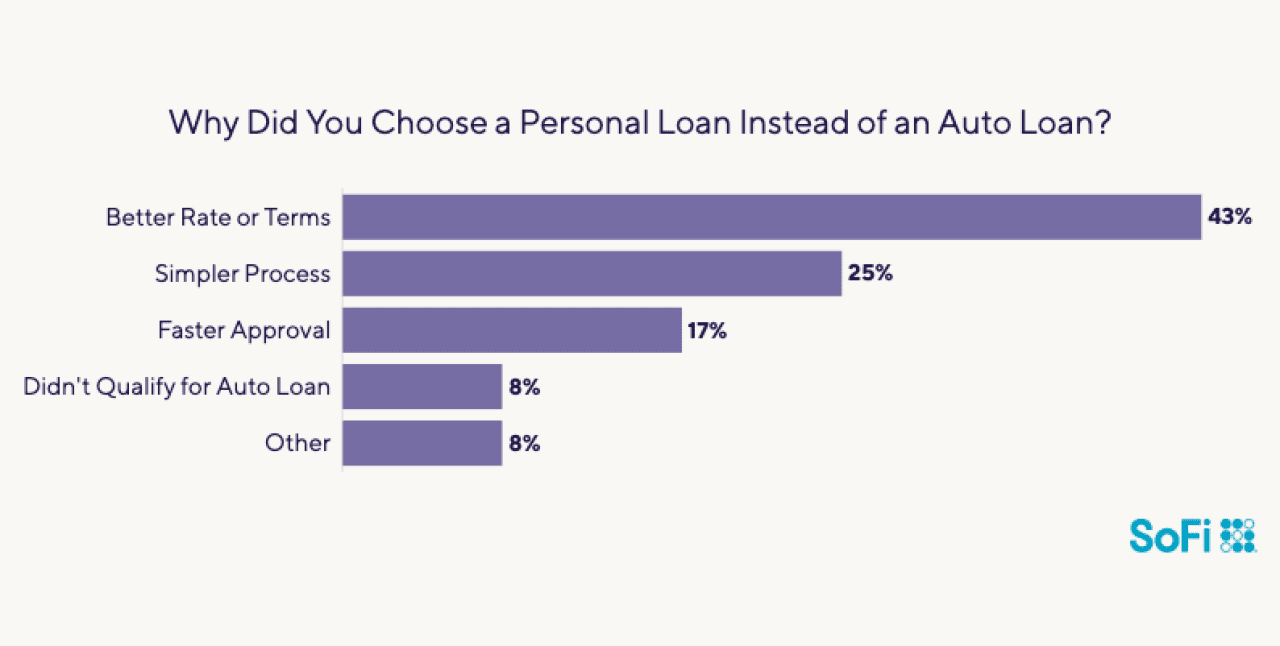

Financing a car with a personal loan can offer some benefits over getting a car loan, including less buyer risk, freedom from a down payment, more power in negotiations, and potential savings on car insurance.

Indeed, among the survey respondents who said they used personal loans for car expenses, 43% said they bypassed auto loans because a personal loan came with better terms and lower rates. One in four felt it was simpler to apply for the personal loan than an auto loan.

SoFi

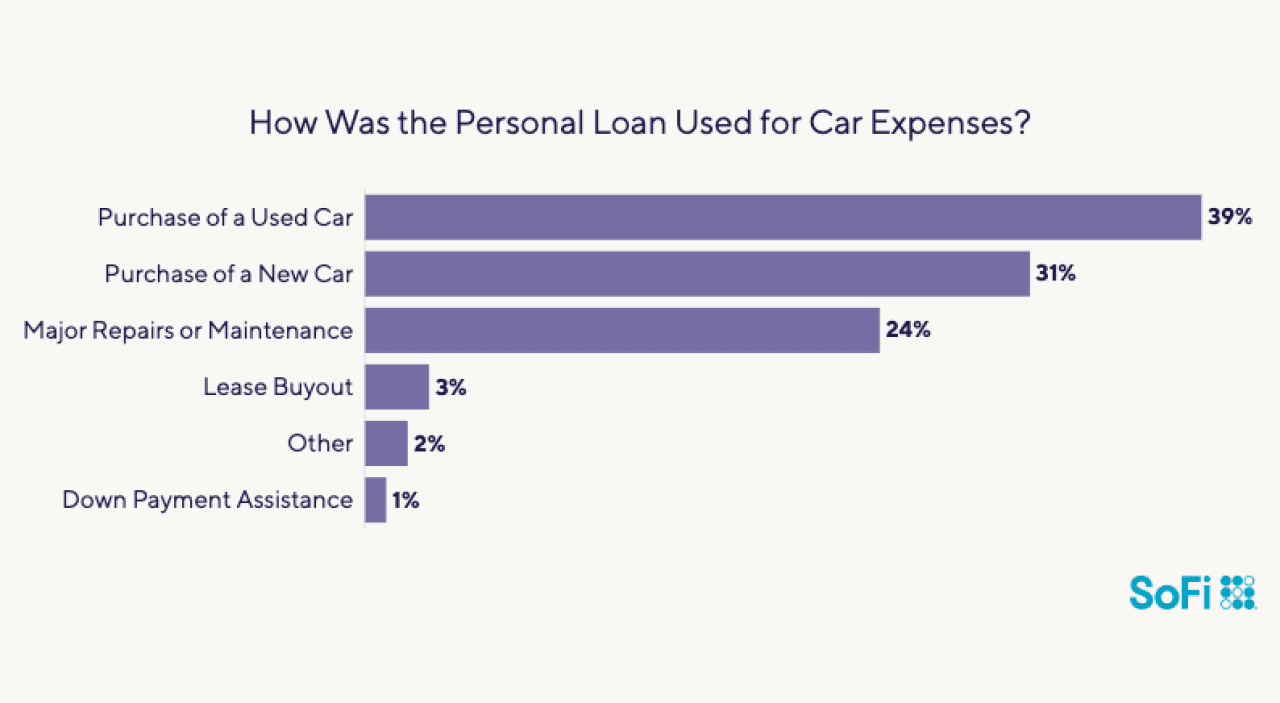

Of those who used their personal loans for automotive costs, 70% said they spent the money to buy a vehicle. More than half of them (or 39% overall) opted for used cars rather than new ones (31% overall). Almost one-quarter (24%) reported they used their loan for major auto repairs.

SoFi

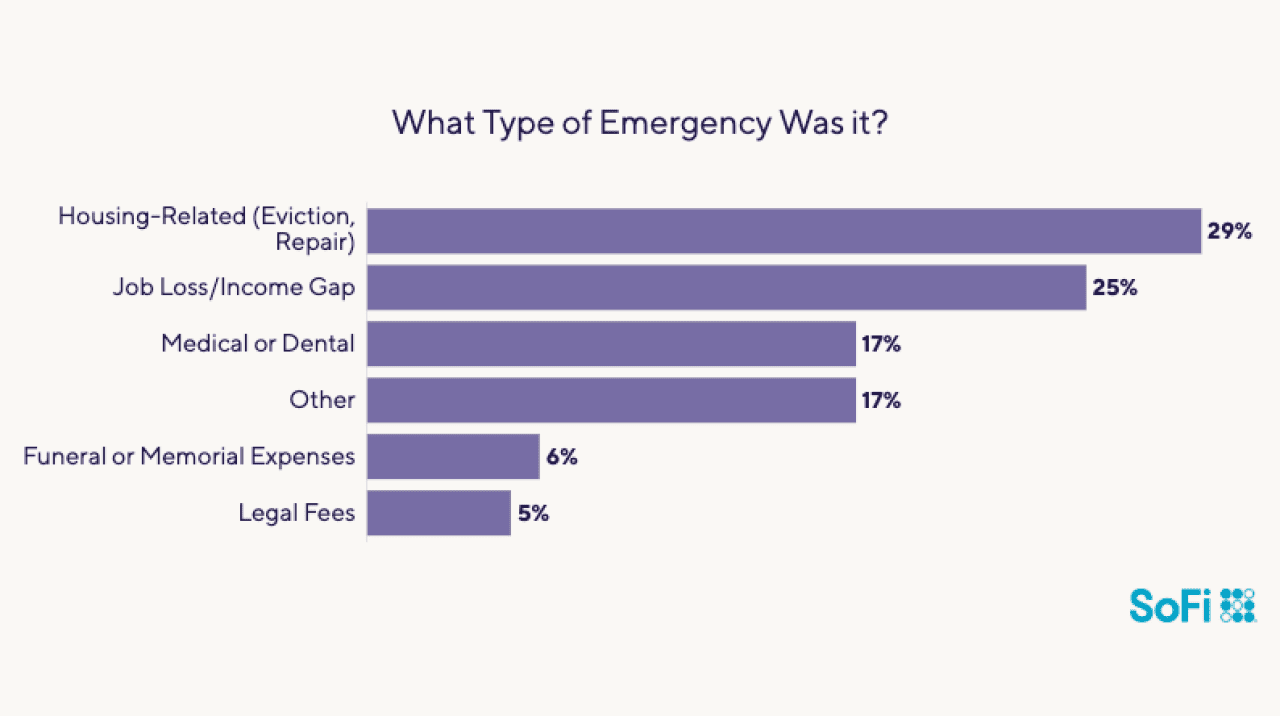

15% Paid Emergency Expenses With Their Loan

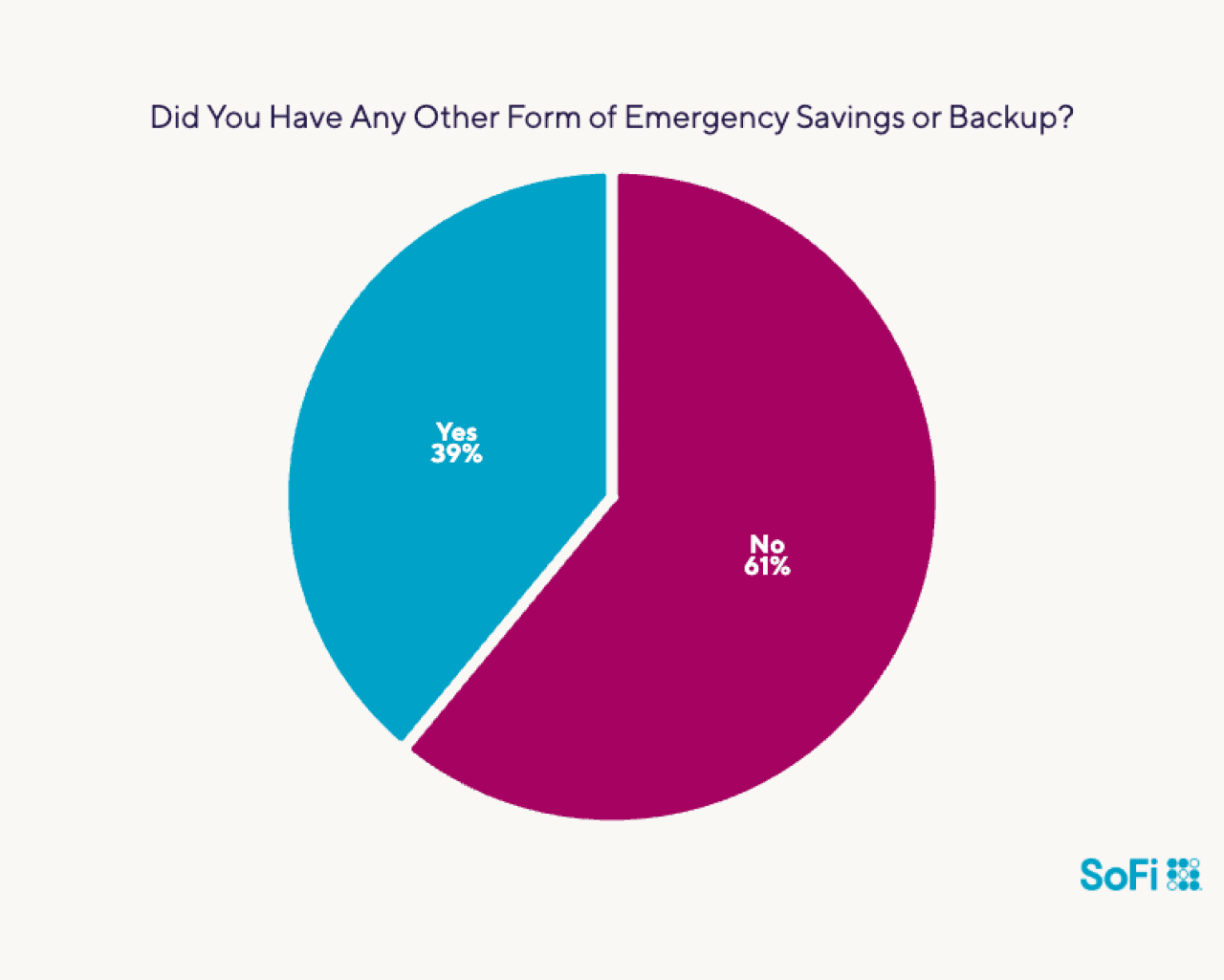

Due to financial uncertainty and the steady squeeze of inflation, Americans’ savings rate has plunged since 2020. The 15% of respondents who used personal loans to deal with emergencies pointed to housing issues (29%), income gaps due to job loss (25%), and medical or dental needs (17%).

More than 60% of this group said they had no rainy-day savings or other financial resources to help them through the emergency.

SoFi

SoFi

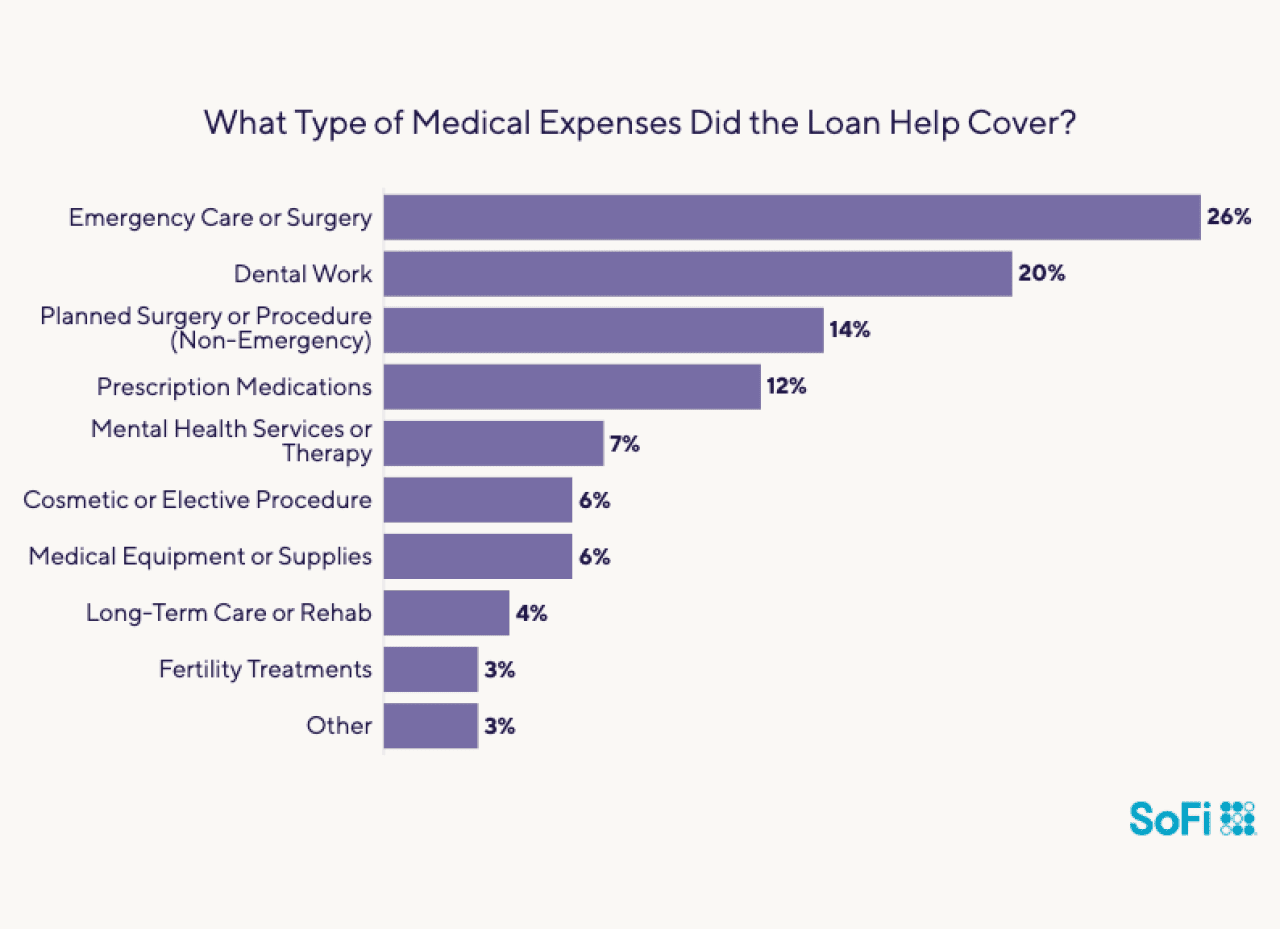

About 14% Used the Loan for Medical or Dental Bills

Even those who have health insurance may not find 100% of medical costs covered, thanks to deductibles and copayments. That may be why 7.6% of all borrowers used personal loans to pay their medical expenses. Of that group, three out of five people specified paying for emergency care, surgery, or dental needs.

An additional 4.1% of all borrowers said they were paying medical bills as part of debt consolidation. Also, of the 17% who used their loans for emergency expenses, about two dozen people (2.6% of all respondents) reported that the emergency involved medical or dental costs.

SoFi

8% of Borrowers Spent Their Loans on Fun Events

Not all personal loans are used for stressful emergencies. Almost 1 in 10 borrowers had positive plans for the cash they received (think a wedding or travel).

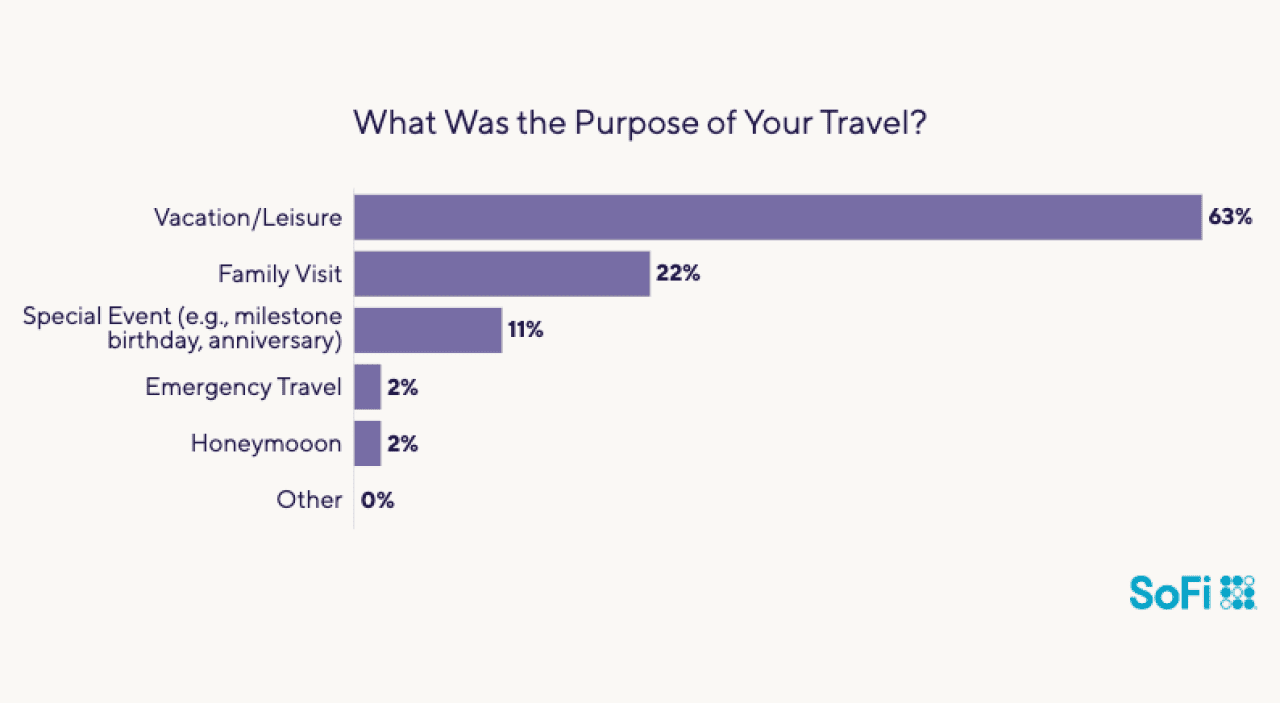

Travel

To help cover travel, 5% of respondents secured vacation loans. Almost two-thirds of this group used their money for leisure travel, and most of the rest (22%) spent their cash on family visits.

SoFi

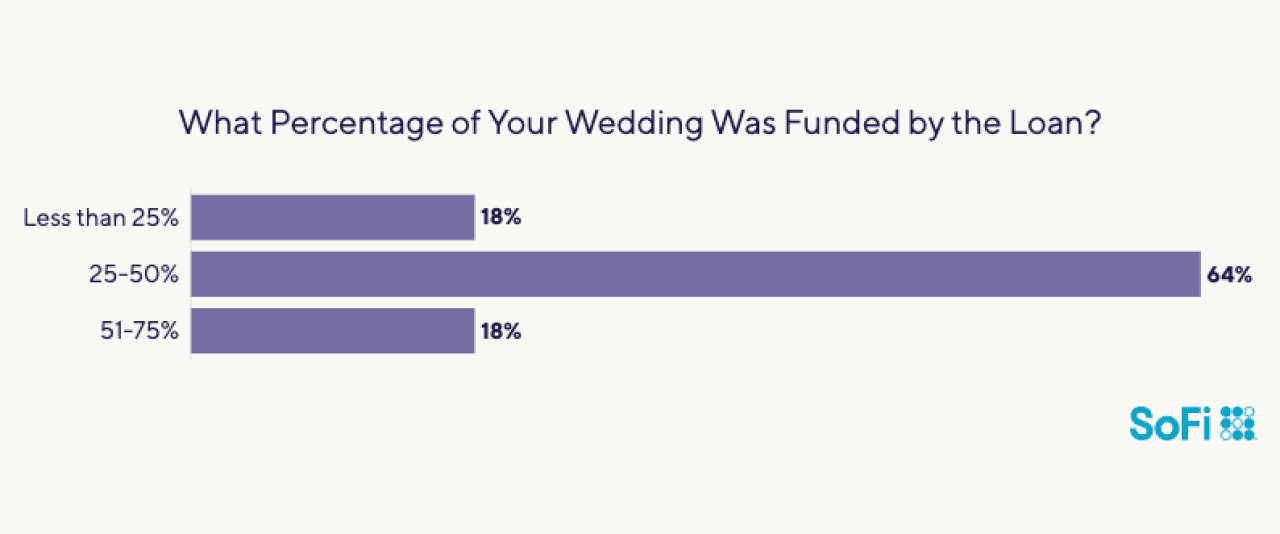

Weddings

The large majority (82%) of those who took out wedding loans borrowed up to half the total cost of their nuptials. For almost two-thirds of all wedding borrowers (64%), the loans paid 25% to 50% of the expenses.

SoFi

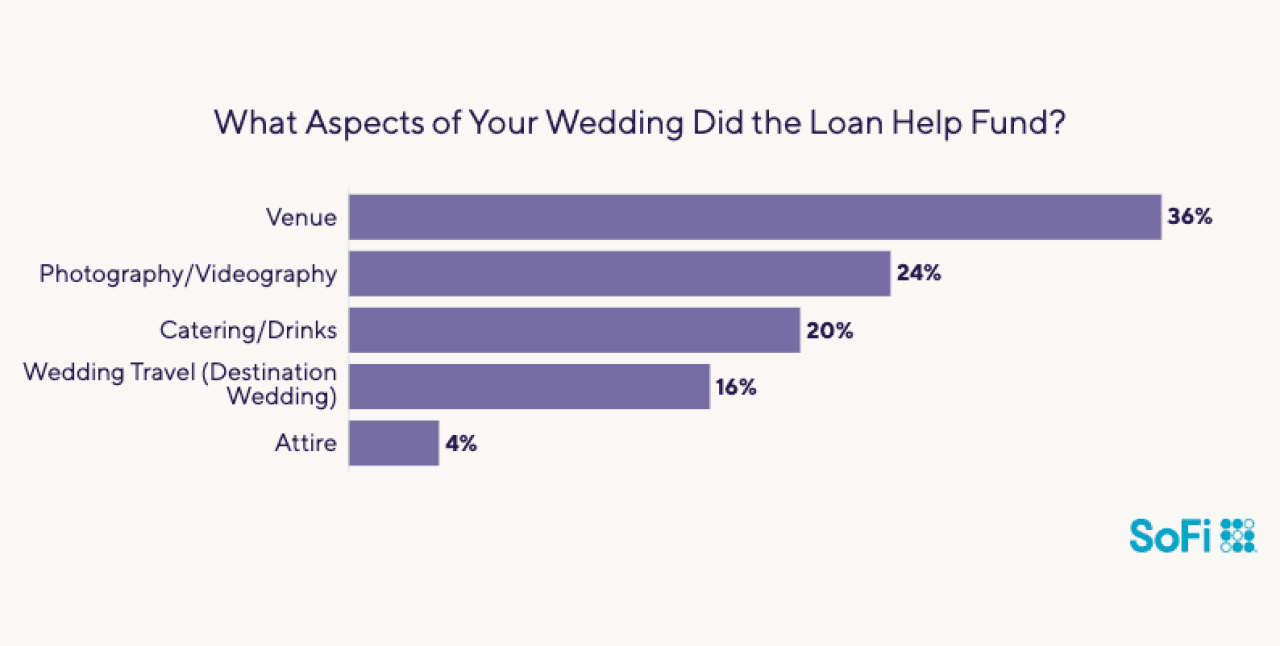

More than 1 in3 couples (36%) put their loan proceeds toward securing the right venue for their ceremony or reception. Almost one quarter (24%) used the money to have the festivities captured on film or video. One in five spent the cash on drinks and catering for their guests.

SoFi

Family Planning

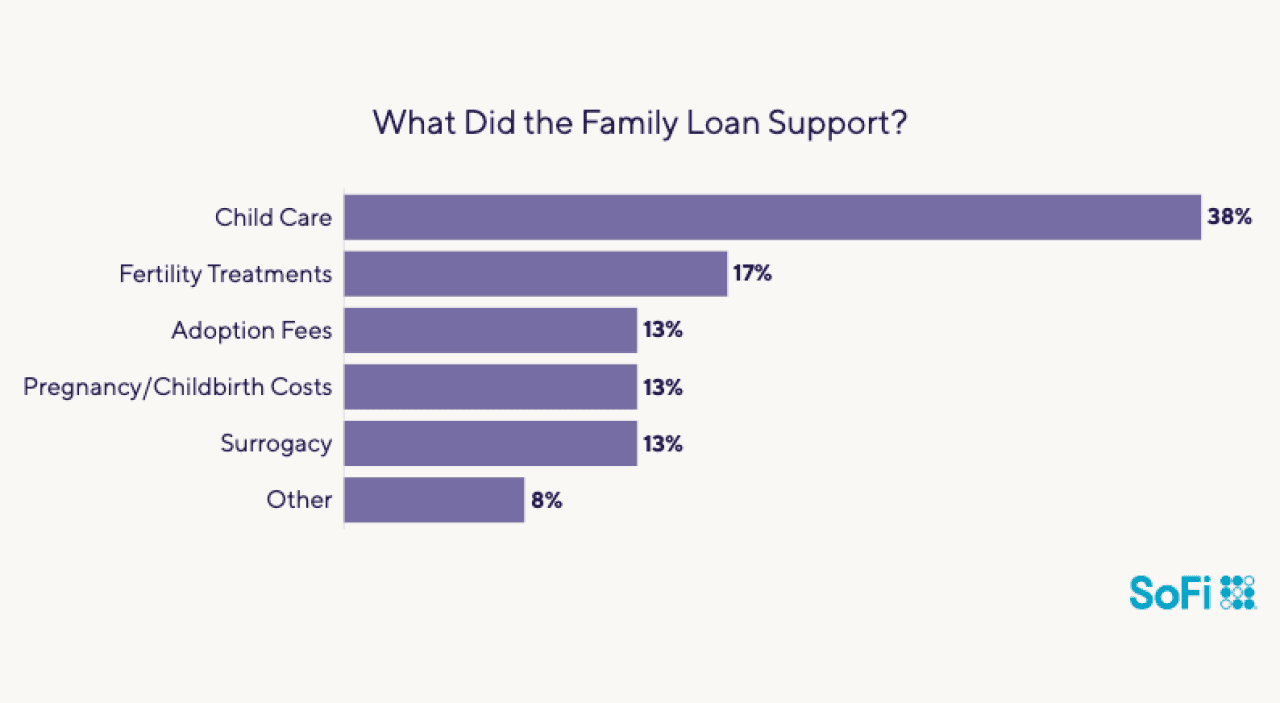

Raising a family is expensive, but only a small share of survey respondents (1.7%) used their most recent personal loan to pay for family planning expenses. Among this group, fertility treatments motivated 17% of borrowers, while 38% cited child care costs.

SoFi

The Borrower Experience

Taking out and then paying off an unsecured personal loan can be a smooth transaction — or it can be bumpy. Many of the survey respondents opted to keep things simple by working with a bank or credit union they were already familiar with. Even so, a majority (58%) of all participants reported issues with high interest rates, monthly payments, or lining up a satisfactory lender.

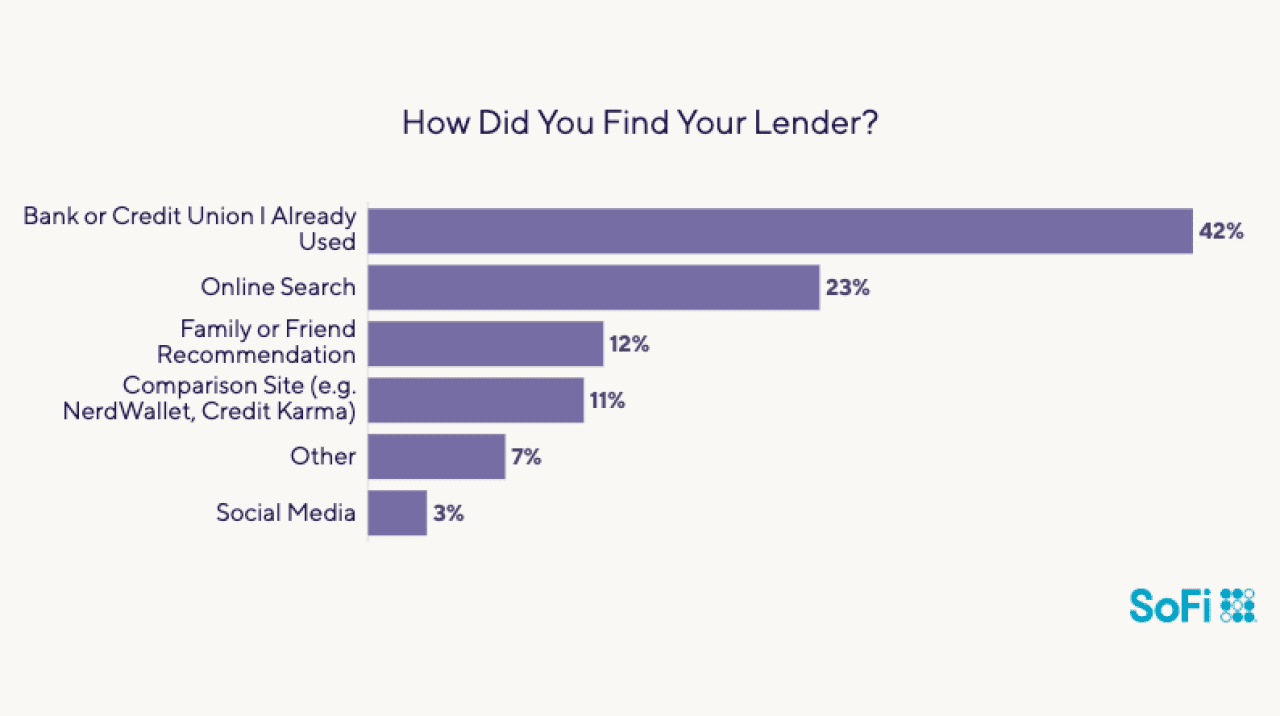

42% Borrowed From Their Current Bank or Credit Union

More than 4 in 10 respondents chose to borrow from a familiar source: the bank or credit union where they already have accounts. This arrangement typically allows for the greatest convenience when making monthly payments.

SoFi

Some borrowers searched farther afield, with 10% of all respondents saying that choosing the right lender was the hardest part of their loan experience.

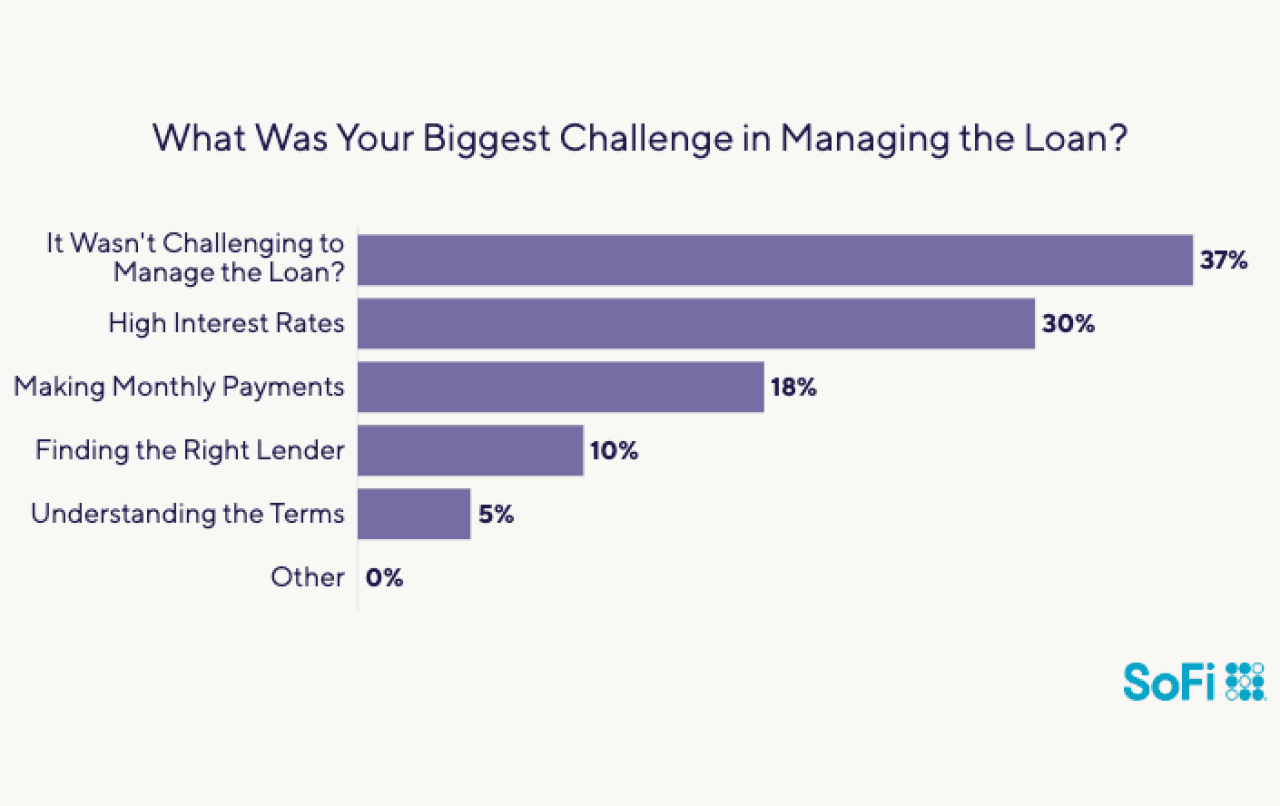

37% Said It Was Easy to Manage Their Loan

SoFi

Borrowers with fixed income often found their personal loans’ unvarying monthly payments to be manageable. In the survey, most retirees with loans (58%) said that it was not a challenge to manage their personal loans. Employed workers were far less likely to say that, whether they work part-time (29%) or full-time (32%).

30% Cited High Interest Rates as Their Biggest Challenge

Three in 10 participants in the survey said that borrowing costs were the toughest aspect of servicing their loans. Among respondents who found loan management challenging (629 respondents or 63%), almost half (299 or 47.5%) blamed it on high interest rates. This was the case for more than one-third (34%) of full-time workers.

One-third (33.3%) of respondents in the Northeast singled out high interest rates as their biggest challenge.

18% Struggled to Make Monthly Payments

Fewer than 1 in 5 respondents to SoFi’s Personal Loan Survey found payments difficult. The western U.S. represents the largest share of respondents (23.3% or roughly 1 in four) who say they had difficulty making the monthly payments on their personal loan.

2% of Borrowers Defaulted or Went into Collections

Just a handful of respondents ended up being seriously delinquent on their personal loans, leading to default or collection actions against them. Personal loans are typically unsecured, so there’s little risk of losing collateral — but in some cases, borrowers can be sued and have their wages garnished for repayment.

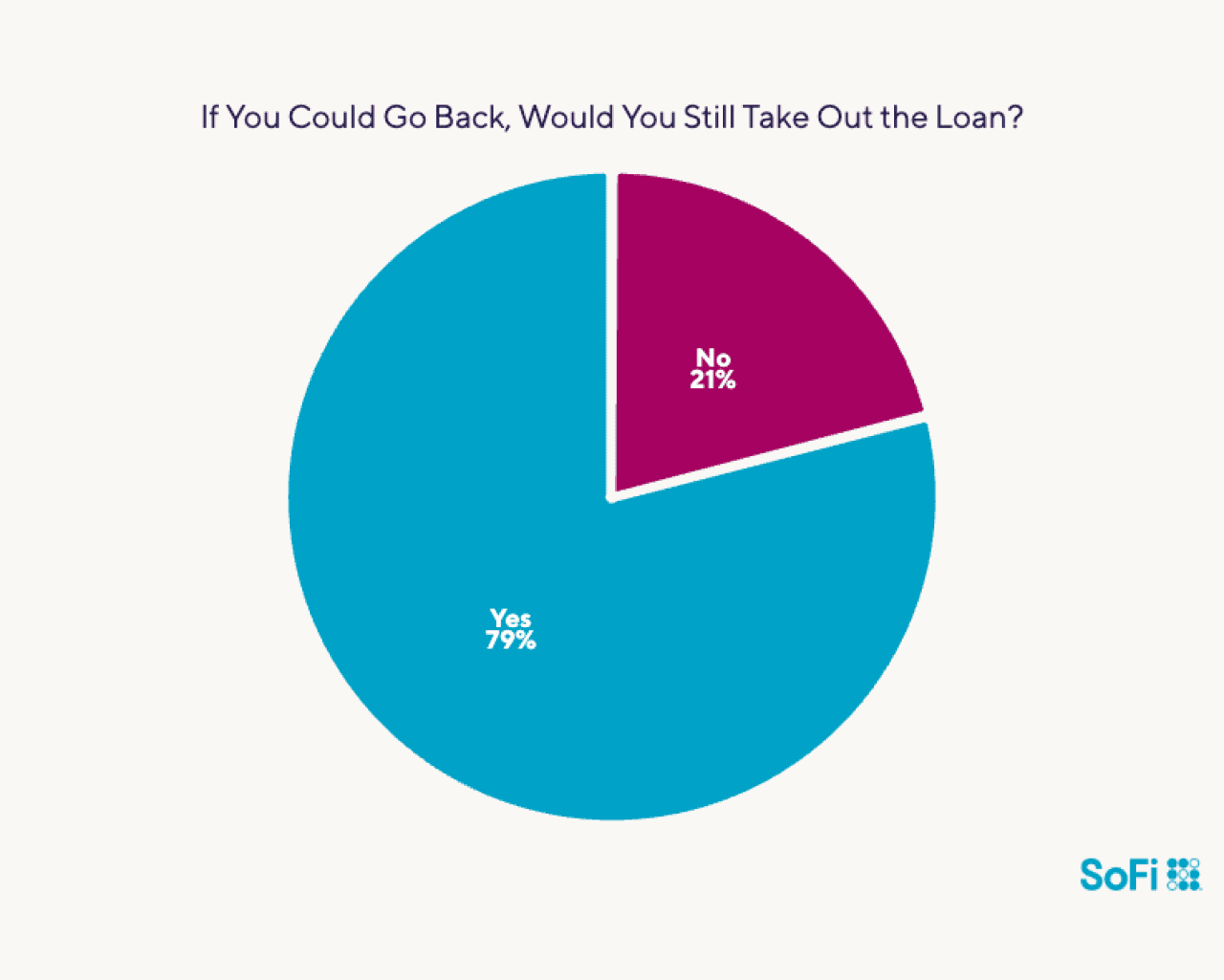

89% of Respondents Were Happy to Use a Loan for Their Chosen Purpose

Almost 90% of people say they have been satisfied with their loan. That said, roughly 11% of borrowers say using a loan for their chosen purpose was a mistake, with 9% saying they “somewhat” regret the loan. And indeed, when asked to consider whether they’d make the same choice again, 21% of all respondents answered “no.”

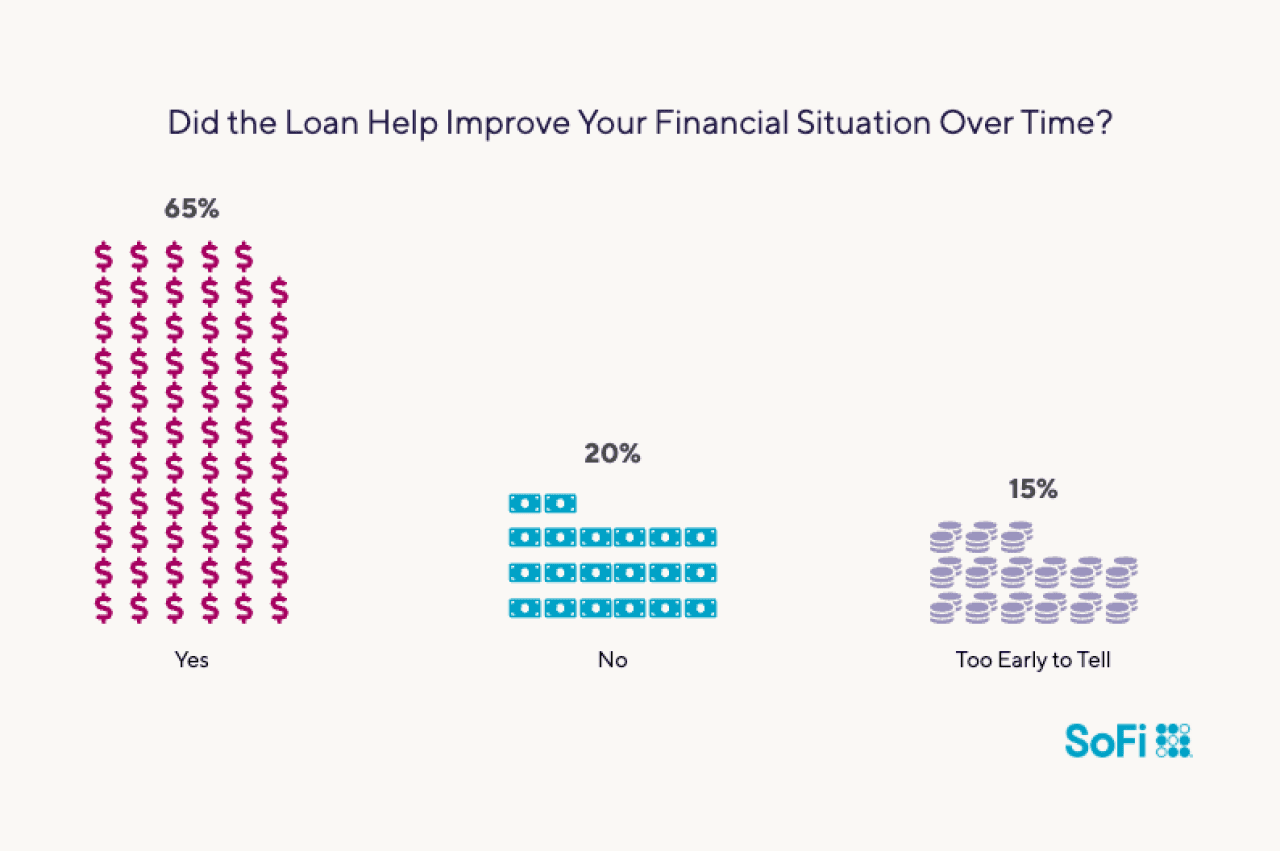

Good News! 65% Are Better Off Financially After Their Most Recent Personal Loan

Almost two-thirds of survey participants said that, over time, their loans helped improve their financial situation. Fifteen percent, or about 1 in 7 people, aren’t ready to make that judgment yet.

SoFi

SoFi

The Takeaway

SoFi’s Real Borrowers, Real Reasons survey sheds light on the who, how, and why aspects of personal loans as 1,000 people revealed their experiences. Most borrowers in the survey were able to secure loan rates well below the national average, which may help explain how 63% of respondents were able to pay off their loans in two years or less. Almost two-thirds concluded that the loan left them in a better financial position, whether they used it for emergency expenses or fun spending.

This story was produced by SoFi and reviewed and distributed by Stacker.

![]()