Is tech making car insurance more expensive?

CC7 // Shutterstock

Is tech making car insurance more expensive?

Backup cameras, adaptive cruise control, self-parking systems, and fully electric engines: Technology has rapidly transformed the auto industry. While these innovations promise greater safety and convenience, they also come with new costs, especially when it comes to insurance. Many drivers are asking a valid question: Is high-tech making car insurance more expensive?

In this article CheapInsurance.com breaks down how modern vehicle technology affects insurance. It examines how insurers calculate rates, the impact of repair costs, and what drivers can do to control their rates in this new age of high-tech cars.

What is Considered High-Tech in Today’s Cars?

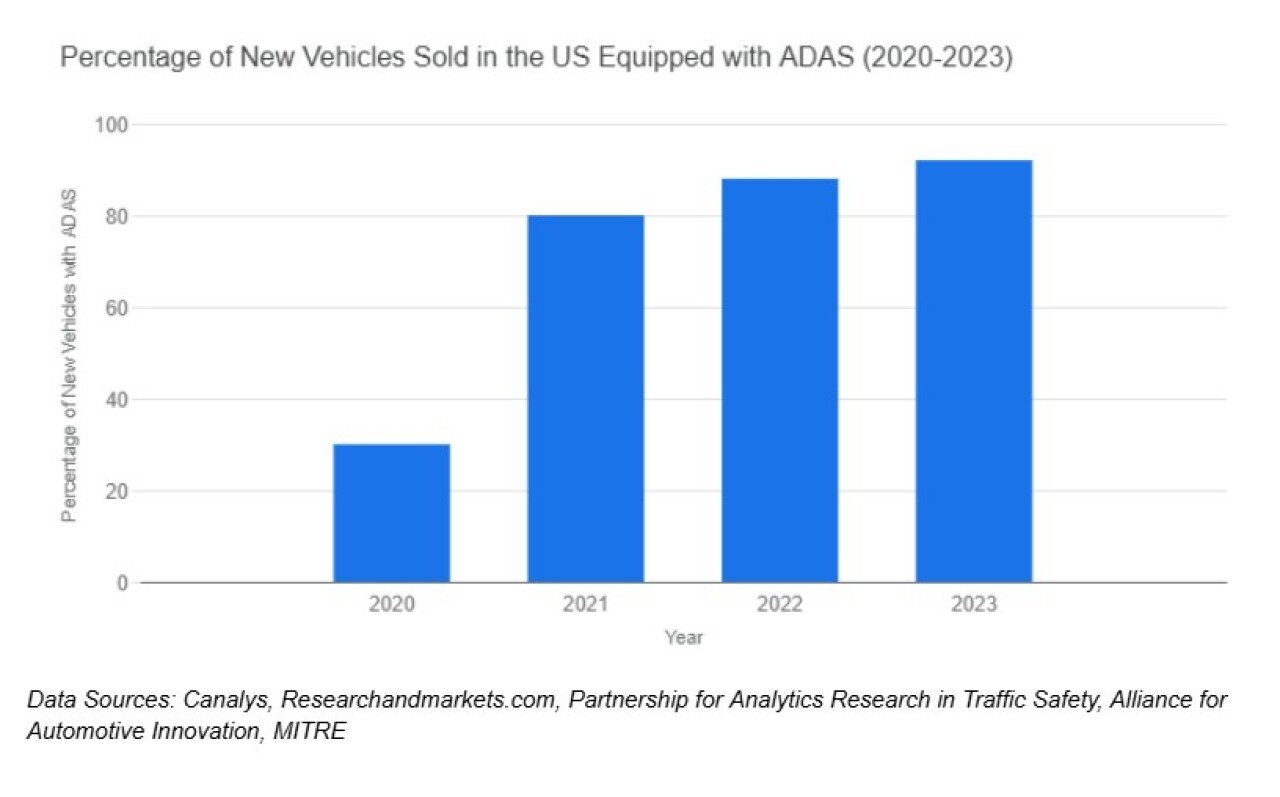

High-tech vehicles don’t just refer to futuristic self-driving cars. Many new features found in standard models today fall under the high-tech category. These include:

- Advanced Driver Assistance Systems (ADAS) like lane departure warnings, blind spot detection, and forward collision alerts.

- Connectivity features, such as GPS tracking, smartphone integration, and real-time diagnostics.

- Electric and hybrid powertrains that replace or supplement internal combustion engines.

- Autonomous features, including self-parking and limited hands-free driving capabilities.

These technologies are designed to improve safety, comfort, and fuel efficiency. But they also introduce new complexities for both repairs and insurance pricing.

CheapInsurance.com

How Do Advanced Features Affect the Cost of Car Insurance?

Insurance companies determine rates based on risk factors, repair costs, vehicle value, and the likelihood of a claim being filed. High-tech features can influence each of these areas.

For example, ADAS systems may help prevent accidents. However, if a vehicle with these systems is involved in a crash, replacing the sensors and cameras involved can be far more expensive than traditional repairs.

Insurance providers take these risks into account. Even if the features reduce the frequency of accidents, the potential cost to repair or replace them is factored into your insurance rate. As a result, the more advanced features your car has, the more you might pay in insurance.

Are Repairs for High-Tech Vehicles Driving Up Insurance Rates?

Yes, the cost of repairing a high-tech car is usually higher than fixing a traditional vehicle. For instance, replacing a standard bumper may cost a few hundred dollars. But if the bumper includes sensors or radar equipment, that same repair can run into the thousands.

Some common examples include:

- Windshield replacement on cars with lane-assist or heads-up displays often requires recalibration of cameras.

- Side mirror damage on vehicles with blind spot monitoring costs significantly more to replace.

- Front-end collisions that involve sensors or adaptive cruise control can triple repair costs.

These expensive repairs mean insurers are more likely to charge higher rates for vehicles with such features, even if they reduce accident risk.

Does Technology Make Cars Safer and Reduce Insurance Claims?

In theory, yes. Many of the innovations in modern vehicles are focused on preventing accidents before they happen. Features like automatic emergency braking, adaptive cruise control, and rear cross-traffic alerts are designed to reduce driver error and improve overall road safety.

Studies have shown that vehicles equipped with ADAS are involved in fewer crashes. Fewer accidents could lead to fewer claims, which benefits both drivers and insurers.

However, the safety benefits don’t always translate directly to lower insurance costs. While the number of claims might decrease, the cost per claim tends to go up due to the expensive technology involved. This trade-off means some drivers may not see the savings they expect on their insurance bills.

How Are Insurers Adjusting Pricing for High-Tech Vehicles?

Insurance companies are adapting, but it’s a slow process. Traditionally, insurers base their rates on a combination of historical data, claim frequency, repair costs, and driver profiles. As more high-tech cars hit the roads, insurers are gathering data on how these vehicles perform in real-world conditions.

Some companies are already using telematics. This technology tracks driving habits like speed, braking, and distance driven. This offers usage-based insurance policies. This can benefit safe drivers who own high-tech cars, as insurers can offer discounts for low-risk behavior backed by data.

In addition, insurers are working closely with automakers and repair shops to better understand the costs of fixing modern vehicles. Over time, this collaboration may help normalize pricing and lead to more accurate insurance quotes.

Are Electric Vehicles and Hybrids More Expensive to Insure?

In most cases, yes. Electric vehicles (EVs) and hybrids generally cost more to insure than their gas-powered counterparts. There are a few reasons why.

- Higher purchase price: Insuring a more expensive car naturally comes with higher rates.

- Costly battery systems: If damaged, battery packs are expensive to repair or replace.

- Specialized parts and labor: Not all shops can service EVs, so repair costs may be higher.

- Limited repair history: Many newer EVs don’t have long-term repair data, making it harder for insurers to predict costs accurately.

However, as EV adoption increases and insurers collect more data, rates could stabilize. Some insurers are even beginning to offer EV-specific discounts or policies.

What Can Drivers Do to Manage Car Insurance Costs on High-Tech Cars?

If you own a high-tech vehicle or plan to buy one soon, there are several strategies to help keep your insurance rates under control.

1. Compare Auto Insurance Quotes from Multiple Providers

Every insurer has a different formula for calculating rates. Get quotes from at least three companies and look for ones that offer discounts for safety features or EV ownership.

2. Consider Telematics or Usage-Based Programs

Many insurers offer telematics, or usage-based insurance policies that track your driving habits. If you drive safely and infrequently, you could earn significant savings.

3. Raise Your Deductible

Opting for a higher deductible can lower your monthly rate, as long as you’re financially prepared to cover more upfront in case of a claim.

4. Ask About Safety Feature Discounts

Not all insurers automatically apply discounts for features like anti-lock brakes or adaptive cruise control. Be sure to ask.

5. Bundle Your Policies

Combining your auto insurance with renters or homeowners insurance can often result in a lower rate for both.

6. Keep a Clean Driving Record

Regardless of your car’s technology, a clean driving history is still one of the biggest factors in lowering your insurance rate.

High-tech vehicles offer incredible benefits. From safer driving to fuel efficiency and convenience. But they also come with higher repair costs, more complex components, and in many cases, more expensive insurance rates. As the industry adjusts and gathers more data, insurance pricing may eventually reflect the long-term savings and risk reductions these technologies bring.

For now, drivers need to be proactive. Understanding how technology affects your insurance and taking steps to manage your policy can make owning a high-tech car more affordable. Whether you’re driving a hybrid, an EV, or a feature-rich SUV, smart insurance shopping will help you get affordable auto insurance quotes.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.

![]()