How employee credit cards work

PeopleImages.com – Yuri A // Shutterstock

How employee credit cards work

Employee credit cards let your team make purchases on your company’s behalf using their own physical or virtual copy of your business credit card. They’re a useful tool to help you control spending, earn rewards, and limit or even eliminate employee expense reimbursements.

With employee cards, you can centralize business purchases and monitor spending in real time. In this guide, Ramp explains how employee credit cards work, their benefits for businesses of all sizes, what to look for when choosing a card, and answers to common questions about rolling out employee cards.

What is an employee credit card?

An employee credit card is an authorized payment card that your employees can use to make purchases on your business’s behalf. The card draws from your company’s line of credit, so employees don’t need to use their personal funds for business expenses.

Employee credit cards can help eliminate the need for expense reimbursements and make it easier to track business spending. Some business credit cards, like corporate cards, include other features like custom spending limits and vendor restrictions. These cards also come with expense management features that allow you to automate expense reporting.

How do employee credit cards work?

Employee credit cards connect to your business’s main credit account, and each card links directly to your company’s line of credit. Your team can use these cards for authorized business expenses like travel, office supplies, client meals, or software subscriptions without using their personal funds or requesting expense reimbursements.

The best employee cards come with a card management system that lets you:

- Issue individual cards to your employees based on their spending needs

- Set spending limits for each cardholder or department

- Restrict purchases to specific merchant categories

- Create automated alerts for transactions that exceed certain thresholds

Your business is fully responsible for all charges made on employee cards, and you must pay the balance according to your credit agreement. Many cards offer rewards and perks such as points, miles, or cashback on purchases. These rewards all go to your business, not to individual employees.

Additionally, employees aren’t personally liable for legitimate business expenses charged to these cards, and these transactions don’t impact their personal credit scores.

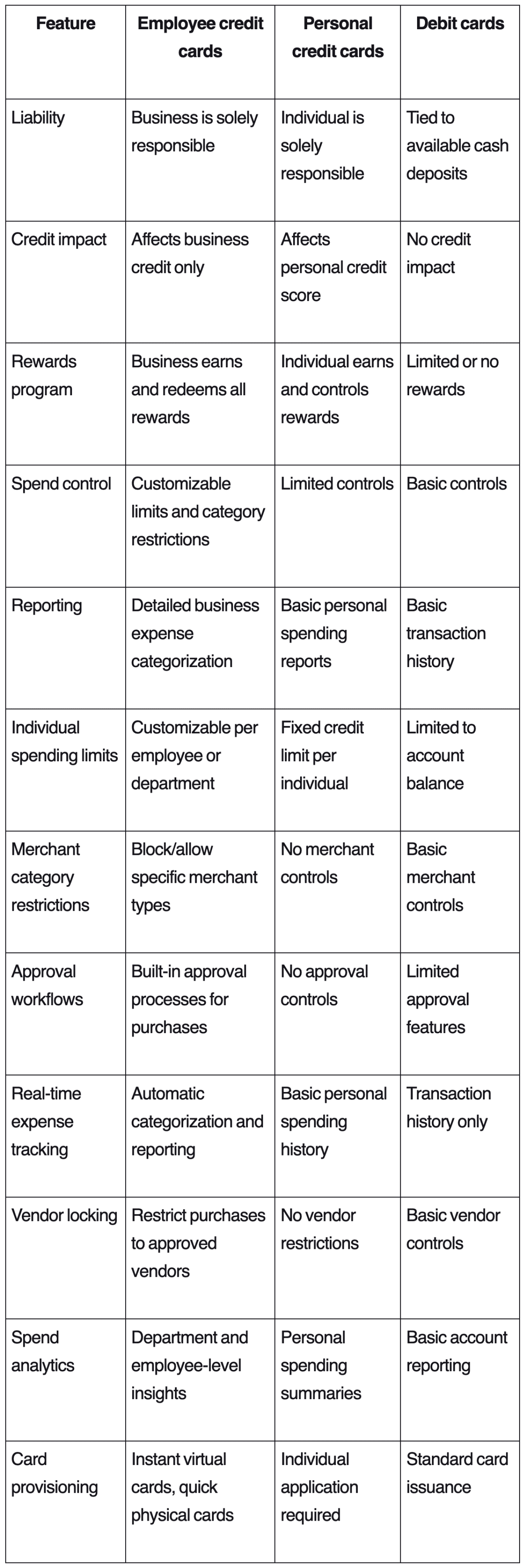

How are employee credit cards different from other cards?

Employee credit cards differ from personal credit cards and other business payment methods in several important ways. They give your employees purchasing freedom while maintaining full control and visibility. This balance lets your team make necessary purchases while giving you the oversight to manage business spending effectively.

Ramp

Key differences that make employee credit cards valuable for small and mid-sized businesses include:

- Your business, not your employees, is responsible for all charges, reducing or even eliminating the need for employee expense reimbursements

- The best employee credit card options come with expense management tools that enable customizable spend limits, vendor and category restrictions, and more

- There’s no impact on your employees’ personal credit, protecting their financial profiles

This setup enables necessary business purchases while maintaining strong oversight.

Corporate credit cards vs. small business credit cards

Corporate credit cards are typically for larger companies with established credit histories and significant annual revenues. These cards offer:

- Higher average credit limits

- Advanced expense management systems

- Sometimes no personal guarantee from business owners

Small business credit cards are accessible to smaller operations and newer businesses with lower revenue and thinner credit history. They usually have:

- More modest credit limits

- A personal credit check and personal guarantee are required from the business owner

- Rewards programs tailored to typical small business spending, like office supplies, telecom, and shipping

Small business cards typically provide basic expense management features, while corporate cards deliver enterprise-level reporting and integration with accounting software or enterprise resource planning (ERP) systems.

Benefits of employee credit cards for businesses

Employee credit cards offer several advantages that make your financial operations more efficient. The main benefits include better expense management, stronger spending control, consolidated rewards, enhanced fraud protection, and greater operational flexibility.

Streamlined expense tracking and reporting

Employee credit cards automatically capture and categorize transaction data, creating digital records of all purchases. This automation eliminates manual entry and frees your employees from filling out expense reports or waiting for reimbursement.

The digital transaction trail reduces errors and provides a complete, accurate record for your finance and accounting teams. At month-end, they can quickly reconcile expenses without chasing down missing receipts, saving hours of administrative work.

More control and visibility over employee expenses

Modern employee card programs give you customizable spending parameters, letting you:

- Set individual spending limits based on employee roles or departments. For example, a manager can issue cards to sales representatives with $2,000 monthly limits for client entertainment and travel, where transactions that would exceed their remaining budget get declined automatically.

- Restrict purchases to specific vendors or merchant categories. Your marketing team can use their cards for advertising platforms like Google Ads and Facebook, but purchases at electronics stores or gas stations get blocked to prevent accidental personal purchases.

- Implement approval workflows for transactions above a certain limit. Any employee transaction over $1,000 triggers an automatic approval request to their manager, who can approve or deny it through the card management platform within minutes.

- Enforce your business’s expense policy automatically. For instance, if your policy prohibits personal purchases, the system can decline transactions at grocery stores or gas stations while allowing office supply purchases.

Real-time transaction alerts notify you of out-of-policy purchases, allowing immediate intervention. In some cases, these controls can even help prevent unauthorized spending before it happens. For example, you might allow your marketing team to make ad purchases but block spending at bars and restaurants.

Reduce fraud and misuse

Employee credit cards include multiple layers of protection against fraud and misuse. Card issuers provide zero-liability policies for unauthorized transactions, and advanced fraud detection systems flag suspicious activity in real time.

You can immediately freeze or cancel physical cards if they’re lost, stolen, or when employees leave. Additionally, many modern employee card options offer the ability to spin up virtual cards for one-off or highly specific purchasing needs, reducing the risk of fraud even further.

Earn rewards on employee spending

By consolidating employee purchases onto company cards, you can maximize rewards. These rewards accumulate in your business account and can add up quickly.

Some cards offer points or miles-based rewards on eligible purchases, while others offer cashback. Certain employee cards may give you higher rewards rates in specific categories as well. You can then redeem rewards for statement credits, business travel, or exclusive business services and discounts.

What to look for in an employee credit card

When choosing employee credit cards, consider factors that affect both financial value and operational efficiency. The right card should balance cost, rewards, expense management features, and integration capabilities to fit your business needs.

- Unlimited cards: Look for options that offer free unlimited physical and virtual cards for authorized users. Some providers charge fees for each additional card, and others may not offer virtual cards.

- Spending controls: Some cards allow you to create employee spending limits, and more advanced cards let you set vendor and expense category restrictions. These limits can reduce business expenses by ensuring cardholders follow your spending policy.

- Real-time tracking: Some providers let you track spending on corporate credit cards in real time. This means you always have an accurate view of how your actual spend is tracking against projected budgets.

- Annual fees and interest rates: Cards with annual fees often provide enhanced rewards and premium perks like airport lounge access. If you plan to carry a balance from month to month, be sure to research the APR for your chosen card. To avoid interest charges, set policies requiring balances to be paid in full each billing cycle.

- Rewards structure: Look for cards that match your spending patterns. Some offer a flat cashback rate on all purchases, while others provide higher rewards in specific categories. Some cards also feature rotating bonus points categories or anniversary bonuses, which can boost your return.

Ideally, the company card you choose should be able to integrate with your business accounting software. Cards that sync automatically with platforms like QuickBooks, Xero, or Sage Intacct reduce manual data entry and reconciliation.

Modern solutions can automatically categorize transactions, attach digital receipts, and generate expense reports. This seamless data flow saves time, improves reporting accuracy, and simplifies tax prep and audits.

Best practices for issuing company credit cards to employees

Before you begin issuing employee cards, make sure you consider factors like training employees, auditing transactions, and tracking and reporting on spending

- Create a clear policy: Write a comprehensive corporate credit card policy that outlines approved purchases, documentation requirements, and consequences for misuse.

- Training: Provide annual training to cardholders regarding acceptable use and company expectations, and make your policy readily available for easy reference.

- Regular audits: Implement a schedule for reviewing card activity to identify patterns and look for opportunities to reduce spending.

- Receipt management: Require employees to submit receipts for all transactions, either physically or through a receipt scanner app, so you don’t run afoul of IRS rules.

- Expense reporting: Implement simple processes for employees to categorize and report expenses.

This story was produced by Ramp and reviewed and distributed by Stacker.

![]()